Page 276 - ACFE Fraud Reports 2009_2020

P. 276

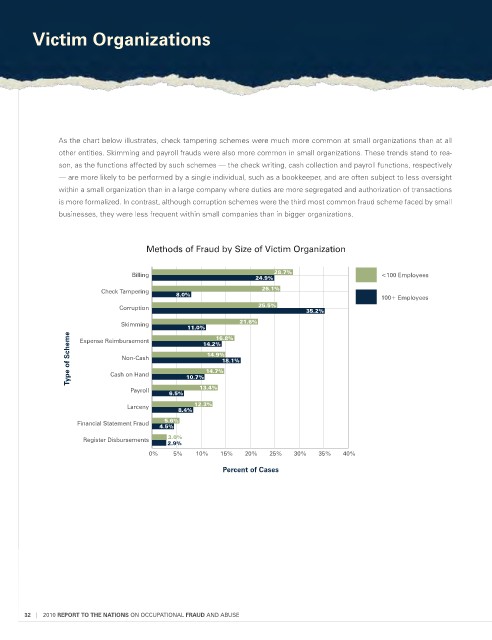

Victim organizations

As the chart below illustrates, check tampering schemes were much more common at small organizations than at all

other entities. Skimming and payroll frauds were also more common in small organizations. These trends stand to rea-

son, as the functions affected by such schemes — the check writing, cash collection and payroll functions, respectively

— are more likely to be performed by a single individual, such as a bookkeeper, and are often subject to less oversight

within a small organization than in a large company where duties are more segregated and authorization of transactions

is more formalized. In contrast, although corruption schemes were the third most common fraud scheme faced by small

businesses, they were less frequent within small companies than in bigger organizations.

Methods of Fraud by Size of Victim Organization

Billing 24.9% 28.7% <100 Employees

Check Tampering 26.1%

8.0%

100+ Employees

Corruption 25.5%

35.2%

Skimming 21.6%

11.0% 16.8%

Type of Scheme Cash on Hand 14.2% 18.1%

Expense Reimbursement

14.9%

Non-Cash

14.7%

13.4%

Payroll 10.7%

6.5%

Larceny 12.3%

8.4%

Financial Statement Fraud 5.6%

4.5%

Register Disbursements 3.0%

2.9%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Percent of Cases

32 | 2010 RepoRt to the NAtioNs ON OccuPATIONAl FRAUD ANd AbuSE