Page 307 - ACFE Fraud Reports 2009_2020

P. 307

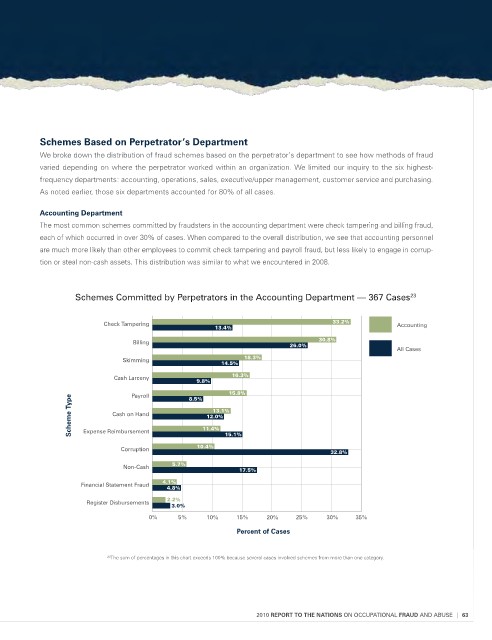

schemes Based on perpetrator’s Department

We broke down the distribution of fraud schemes based on the perpetrator’s department to see how methods of fraud

varied depending on where the perpetrator worked within an organization. We limited our inquiry to the six highest-

frequency departments: accounting, operations, sales, executive/upper management, customer service and purchasing.

As noted earlier, those six departments accounted for 80% of all cases.

Accounting Department

The most common schemes committed by fraudsters in the accounting department were check tampering and billing fraud,

each of which occurred in over 30% of cases. When compared to the overall distribution, we see that accounting personnel

are much more likely than other employees to commit check tampering and payroll fraud, but less likely to engage in corrup-

tion or steal non-cash assets. This distribution was similar to what we encountered in 2008.

Schemes committed by Perpetrators in the Accounting department — 367 cases 23

Check Tampering 33.2% Accounting

13.4%

Billing 30.8%

26.0%

All Cases

Skimming 18.3%

14.5%

16.3%

Cash Larceny 9.8% 15.8%

Payroll

Scheme Type Expense Reimbursement 8.5% 11.4%

13.1%

Cash on Hand

12.0%

Corruption 10.4% 15.1% 32.8%

Non-Cash 5.7% 17.5%

Financial Statement Fraud 4.1%

4.8%

Register Disbursements 2.2%

3.0%

0% 5% 10% 15% 20% 25% 30% 35%

Percent of Cases

23 The sum of percentages in this chart exceeds 100% because several cases involved schemes from more than one category.

2010 RepoRt to the NAtioNs ON OccuPATIONAl FRAUD ANd AbuSE | 63