Page 364 - ACFE Fraud Reports 2009_2020

P. 364

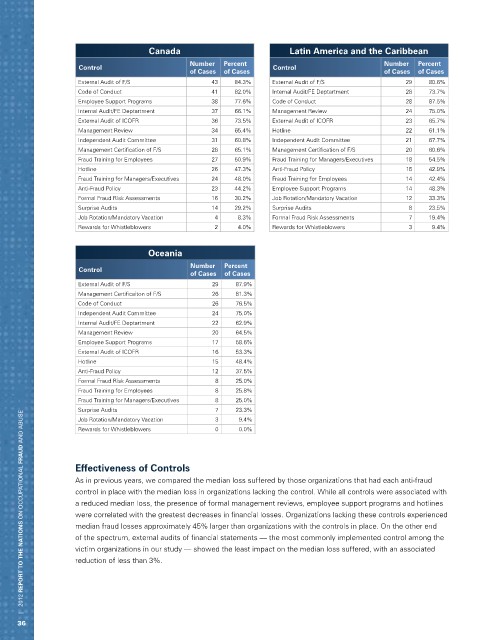

Canada Latin America and the Caribbean

Number Percent Number Percent

Control Control

of Cases of Cases of Cases of Cases

External Audit of F/S 43 84.3% External Audit of F/S 29 80.6%

Code of Conduct 41 82.0% Internal Audit/FE Deptartment 28 73.7%

Employee Support Programs 38 77.6% Code of Conduct 28 87.5%

Internal Audit/FE Deptartment 37 66.1% Management Review 24 75.0%

External Audit of ICOFR 36 73.5% External Audit of ICOFR 23 65.7%

Management Review 34 65.4% Hotline 22 61.1%

Independent Audit Committee 31 60.8% Independent Audit Committee 21 67.7%

Management Certification of F/S 28 65.1% Management Certification of F/S 20 60.6%

Fraud Training for Employees 27 50.9% Fraud Training for Managers/Executives 18 54.5%

Hotline 26 47.3% Anti-Fraud Policy 15 42.9%

Fraud Training for Managers/Executives 24 48.0% Fraud Training for Employees 14 42.4%

Anti-Fraud Policy 23 44.2% Employee Support Programs 14 48.3%

Formal Fraud Risk Assessments 16 30.2% Job Rotation/Mandatory Vacation 12 33.3%

Surprise Audits 14 29.2% Surprise Audits 8 23.5%

Job Rotation/Mandatory Vacation 4 8.3% Formal Fraud Risk Assessments 7 19.4%

Rewards for Whistleblowers 2 4.0% Rewards for Whistleblowers 3 9.4%

Oceania

Number Percent

Control

of Cases of Cases

External Audit of F/S 29 87.9%

Management Certificaiton of F/S 26 81.3%

Code of Conduct 26 76.5%

Independent Audit Committee 24 75.0%

Internal Audit/FE Deptartment 22 62.9%

Management Review 20 64.5%

Employee Support Programs 17 58.6%

External Audit of ICOFR 16 53.3%

Hotline 15 48.4%

Anti-Fraud Policy 12 37.5%

Formal Fraud Risk Assessments 8 25.0%

Fraud Training for Employees 8 25.8%

Fraud Training for Managers/Executives 8 25.0%

Surprise Audits 7 23.3%

| 2012 REPORT TO THE NATIONS on occupational FRAUD and abuse

Job Rotation/Mandatory Vacation 3 9.4%

Rewards for Whistleblowers 0 0.0%

Effectiveness of Controls

As in previous years, we compared the median loss suffered by those organizations that had each anti-fraud

control in place with the median loss in organizations lacking the control. While all controls were associated with

a reduced median loss, the presence of formal management reviews, employee support programs and hotlines

were correlated with the greatest decreases in financial losses. Organizations lacking these controls experienced

median fraud losses approximately 45% larger than organizations with the controls in place. On the other end

of the spectrum, external audits of financial statements — the most commonly implemented control among the

victim organizations in our study — showed the least impact on the median loss suffered, with an associated

reduction of less than 3%.

36