Page 41 - ACFE Fraud Reports 2009_2020

P. 41

D E T E C T I N G & P R E V E N T I N G F R A U D

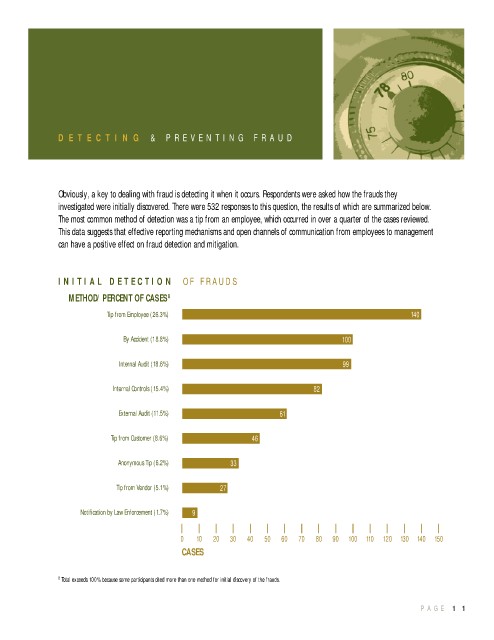

Obviously, a key to dealing with fraud is detecting it when it occurs. Respondents were asked how the frauds they

investigated were initially discovered. There were 532 responses to this question, the results of which are summarized below.

The most common method of detection was a tip from an employee, which occurred in over a quarter of the cases reviewed.

This data suggests that effective reporting mechanisms and open channels of communication from employees to management

can have a positive effect on fraud detection and mitigation.

I N I T I A L D E T E C T I O N O F F R A U D S

METHOD/PERCENT OF CASES 8

Tip from Employee (26.3%) 140

By Accident (18.8%) 100

Internal Audit (18.6%) 99

Internal Controls (15.4%) 82

External Audit (11.5%) 61

Tip from Customer (8.6%) 46

Anonymous Tip (6.2%) 33

Tip from Vendor (5.1%) 27

Notification by Law Enforcement (1.7%) 9

0 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150

CASES

8 Total exceeds 100% because some participants cited more than one method for initial discovery of the frauds.

P A G E 1 1