Page 417 - ACFE Fraud Reports 2009_2020

P. 417

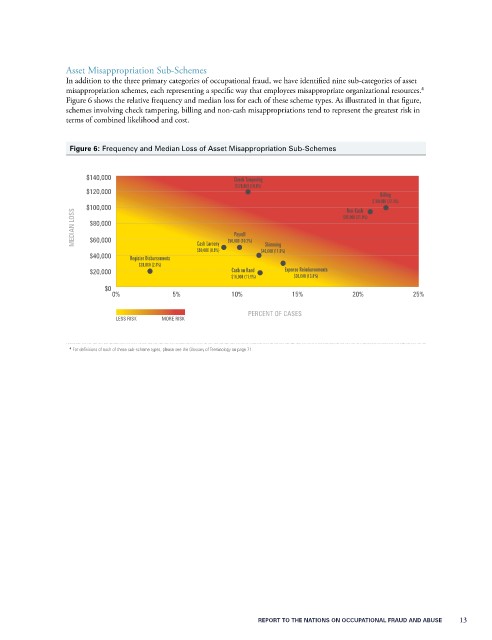

Asset Misappropriation Sub-Schemes

In addition to the three primary categories of occupational fraud, we have identified nine sub-categories of asset

4

misappropriation schemes, each representing a specific way that employees misappropriate organizational resources.

Figure 6 shows the relative frequency and median loss for each of these scheme types. As illustrated in that figure,

schemes involving check tampering, billing and non-cash misappropriations tend to represent the greatest risk in

terms of combined likelihood and cost.

Figure 6: Frequency and Median Loss of Asset Misappropriation Sub-Schemes

$140,000 Check Tampering

$120,000 (10.9%)

$120,000

Billing

$100,000 (22.3%)

$100,000 $95,000 (21.0%)

Non-Cash

MEDIAN LOSS $80,000 Payroll

$60,000

Cash Larceny

Skimming

$50,000 (8.9%) $50,000 (10.2%) $40,000 (11.8%)

$40,000 Register Disbursements

$20,000 (2.8%)

$20,000 Cash on Hand Expense Reimbursements

$18,000 (11.9%) $30,000 (13.8%)

$0

0% 5% 10% 15% 20% 25%

PERCENT OF CASES

LESS RISK MORE RISK

4 For definitions of each of these sub-scheme types, please see the Glossary of Terminology on page 71.

RepoRt to the NatioNs oN occupatioNal FRaud aNd abuse 13