Page 419 - ACFE Fraud Reports 2009_2020

P. 419

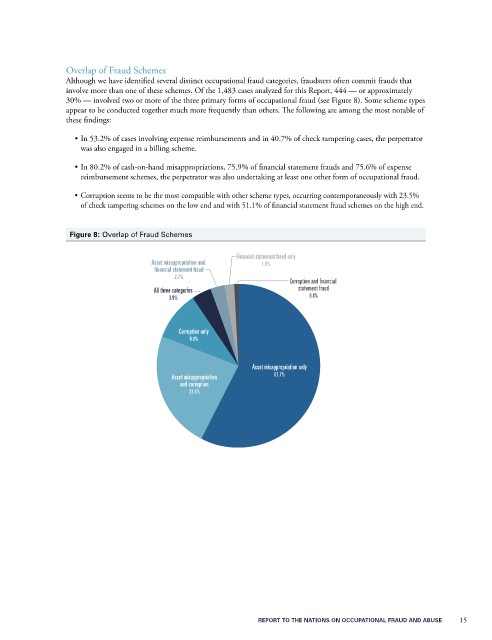

Overlap of Fraud Schemes

Although we have identified several distinct occupational fraud categories, fraudsters often commit frauds that

involve more than one of these schemes. Of the 1,483 cases analyzed for this Report, 444 — or approximately

30% — involved two or more of the three primary forms of occupational fraud (see Figure 8). Some scheme types

appear to be conducted together much more frequently than others. The following are among the most notable of

these findings:

• In 53.2% of cases involving expense reimbursements and in 40.7% of check tampering cases, the perpetrator

was also engaged in a billing scheme.

• In 80.2% of cash-on-hand misappropriations, 75.9% of financial statement frauds and 75.6% of expense

reimbursement schemes, the perpetrator was also undertaking at least one other form of occupational fraud.

• Corruption seems to be the most compatible with other scheme types, occurring contemporaneously with 23.5%

of check tampering schemes on the low end and with 51.1% of financial statement fraud schemes on the high end.

Figure 8: Overlap of Fraud Schemes

Financial statement fraud only

Asset misappropriation and 1.8%

financial statement fraud

2.7%

Corruption and financial

All three categories statement fraud

3.9% 0.8%

Corruption only

9.8%

Asset misappropriation only

Asset misappropriation 57.7%

and corruption

23.3%

6.6% 2.9%

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 15