Page 423 - ACFE Fraud Reports 2009_2020

P. 423

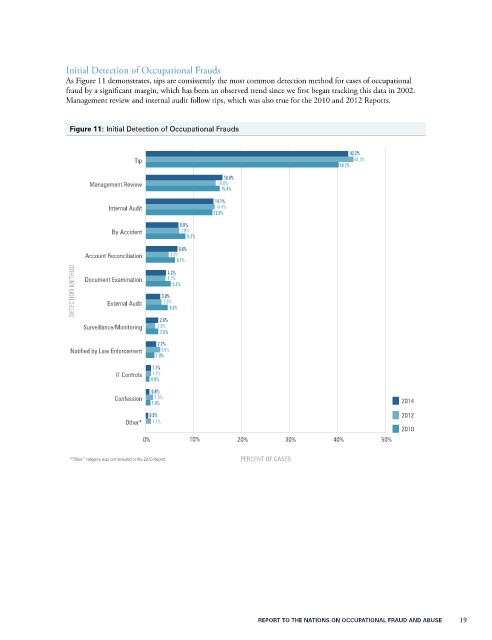

Initial Detection of Occupational Frauds

As Figure 11 demonstrates, tips are consistently the most common detection method for cases of occupational

fraud by a significant margin, which has been an observed trend since we first began tracking this data in 2002.

Management review and internal audit follow tips, which was also true for the 2010 and 2012 Reports.

Figure 11: Initial Detection of Occupational Frauds

42.2%

Tip 43.3%

40.2%

16.0%

Management Review 14.6%

15.4%

14.1%

Internal Audit 14.4%

13.9%

6.8%

By Accident 7.0%

8.3%

6.6%

Account Reconciliation 4.8%

6.1%

DETECTION METHOD Document Examination 3.0% 4.1% 5.2%

4.2%

3.3%

External Audit

2.6% 4.6%

Surveillance/Monitoring 1.9%

2.6%

2.2%

Notified by Law Enforcement 3.0%

1.8%

1.1%

IT Controls 1.1%

0.8%

0.8%

Confession 1.5% 2014

1.0%

0.5% 2012

Other* 1.1%

2010

0% 10% 20% 30% 40% 50%

*“Other” category was not included in the 2010 Report. PERCENT OF CASES

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 19