Page 426 - ACFE Fraud Reports 2009_2020

P. 426

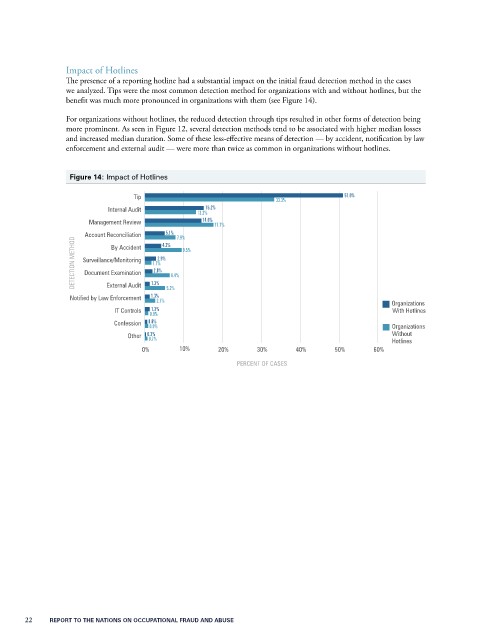

Impact of Hotlines

The presence of a reporting hotline had a substantial impact on the initial fraud detection method in the cases

we analyzed. Tips were the most common detection method for organizations with and without hotlines, but the

benefit was much more pronounced in organizations with them (see Figure 14).

For organizations without hotlines, the reduced detection through tips resulted in other forms of detection being

more prominent. As seen in Figure 12, several detection methods tend to be associated with higher median losses

and increased median duration. Some of these less-effective means of detection — by accident, notification by law

enforcement and external audit — were more than twice as common in organizations without hotlines.

Figure 14: Impact of Hotlines

Tip 33.3% 51.0%

Internal Audit 15.2%

13.2%

Management Review 14.6% 17.7%

5.1%

Account Reconciliation 4.2% 7.9%

DETECTION METHOD Surveillance/Monitoring 1.7% 2.9% 6.4% 9.5%

By Accident

2.0%

Document Examination

External Audit

1.3%

Notified by Law Enforcement 1.3% 2.7% 5.2% Organizations

1.3%

IT Controls 0.9% With Hotlines

Confession 0.6% Organizations

0.9%

Other 0.3% Without

0.7%

Hotlines

0% 10% 20% 30% 40% 50% 60%

PERCENT OF CASES

22 REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE