Page 430 - ACFE Fraud Reports 2009_2020

P. 430

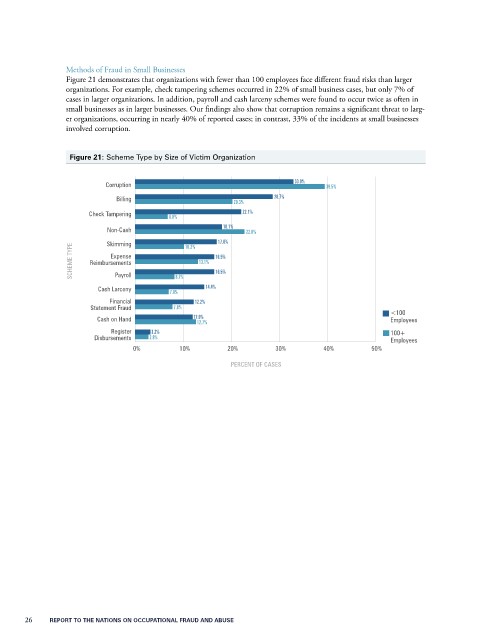

Methods of Fraud in Small Businesses

Figure 21 demonstrates that organizations with fewer than 100 employees face different fraud risks than larger

organizations. For example, check tampering schemes occurred in 22% of small business cases, but only 7% of

cases in larger organizations. In addition, payroll and cash larceny schemes were found to occur twice as often in

small businesses as in larger businesses. Our findings also show that corruption remains a significant threat to larg-

er organizations, occurring in nearly 40% of reported cases; in contrast, 33% of the incidents at small businesses

involved corruption.

Figure 21: Scheme Type by Size of Victim Organization

Corruption 33.0% 39.5%

Billing 28.7%

20.3%

Check Tampering 22.1%

6.8%

18.1%

Non-Cash 17.0% 22.8%

Skimming

SCHEME TYPE Reimbursements 10.2% 13.1% 16.5%

Expense

16.5%

Payroll

Cash Larceny 8.2% 14.4%

7.0%

Financial 12.2%

Statement Fraud 7.8% <100

Cash on Hand 12.0% Employees

12.7%

Register 3.2% 100+

Disbursements 2.8% Employees

0% 10% 20% 30% 40% 50%

PERCENT OF CASES

26 REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE