Page 435 - ACFE Fraud Reports 2009_2020

P. 435

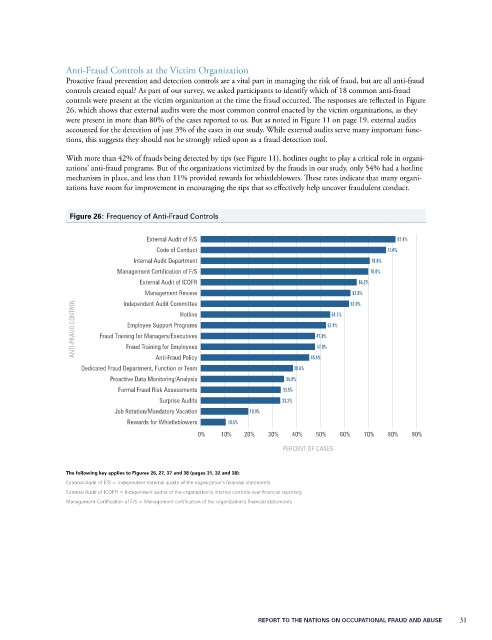

Anti-Fraud Controls at the Victim Organization

Proactive fraud prevention and detection controls are a vital part in managing the risk of fraud, but are all anti-fraud

controls created equal? As part of our survey, we asked participants to identify which of 18 common anti-fraud

controls were present at the victim organization at the time the fraud occurred. The responses are reflected in Figure

26, which shows that external audits were the most common control enacted by the victim organizations, as they

were present in more than 80% of the cases reported to us. But as noted in Figure 11 on page 19, external audits

accounted for the detection of just 3% of the cases in our study. While external audits serve many important func-

tions, this suggests they should not be strongly relied upon as a fraud detection tool.

With more than 42% of frauds being detected by tips (see Figure 11), hotlines ought to play a critical role in organi-

zations’ anti-fraud programs. But of the organizations victimized by the frauds in our study, only 54% had a hotline

mechanism in place, and less than 11% provided rewards for whistleblowers. These rates indicate that many organi-

zations have room for improvement in encouraging the tips that so effectively help uncover fraudulent conduct.

Figure 26: Frequency of Anti-Fraud Controls

External Audit of F/S 81.4%

Code of Conduct 77.4%

Internal Audit Department 70.6%

Management Certification of F/S 70.0%

External Audit of ICOFR 65.2%

Management Review 62.0%

62.6%

Independent Audit Committee

ANTI-FRAUD CONTROL Fraud Training for Managers/Executives 47.8% 52.4%

Hotline

54.1%

Employee Support Programs

Fraud Training for Employees

47.8%

Anti-Fraud Policy

Dedicated Fraud Department, Function or Team 38.6% 45.4%

Proactive Data Monitoring/Analysis 34.8%

Formal Fraud Risk Assessments 33.5%

Surprise Audits 33.2%

Job Rotation/Mandatory Vacation 19.9%

Rewards for Whistleblowers 10.5%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

PERCENT OF CASES

the following key applies to Figures 26, 27, 37 and 38 (pages 31, 32 and 38):

External Audit of F/S = Independent external audits of the organization’s financial statements

External Audit of ICOFR = Independent audits of the organization’s internal controls over financial reporting

Management Certification of F/S = Management certification of the organization’s financial statements

RepoRt to the NatioNs oN occupatioNal FRaud aNd abuse 31