Page 437 - ACFE Fraud Reports 2009_2020

P. 437

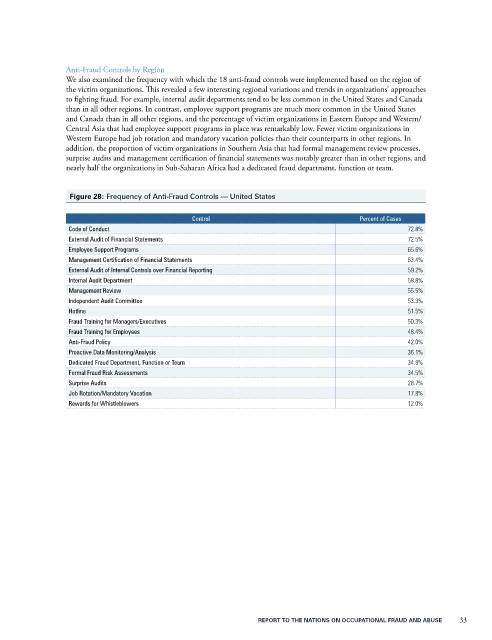

Anti-Fraud Controls by Region

We also examined the frequency with which the 18 anti-fraud controls were implemented based on the region of

the victim organizations. This revealed a few interesting regional variations and trends in organizations’ approaches

to fighting fraud. For example, internal audit departments tend to be less common in the United States and Canada

than in all other regions. In contrast, employee support programs are much more common in the United States

and Canada than in all other regions, and the percentage of victim organizations in Eastern Europe and Western/

Central Asia that had employee support programs in place was remarkably low. Fewer victim organizations in

Western Europe had job rotation and mandatory vacation policies than their counterparts in other regions. In

addition, the proportion of victim organizations in Southern Asia that had formal management review processes,

surprise audits and management certification of financial statements was notably greater than in other regions, and

nearly half the organizations in Sub-Saharan Africa had a dedicated fraud department, function or team.

Figure 28: Frequency of Anti-Fraud Controls — United States

Control Percent of Cases

Code of Conduct 72.8%

External Audit of Financial Statements 72.5%

Employee Support Programs 65.6%

Management Certification of Financial Statements 63.4%

External Audit of Internal Controls over Financial Reporting 59.2%

Internal Audit Department 58.8%

Management Review 55.5%

Independent Audit Committee 53.3%

Hotline 51.5%

Fraud Training for Managers/Executives 50.3%

Fraud Training for Employees 48.4%

Anti-Fraud Policy 42.0%

Proactive Data Monitoring/Analysis 36.1%

Dedicated Fraud Department, Function or Team 34.8%

Formal Fraud Risk Assessments 34.5%

Surprise Audits 28.7%

Job Rotation/Mandatory Vacation 17.8%

Rewards for Whistleblowers 12.0%

RepoRt to the NatioNs oN occupatioNal FRaud aNd abuse 33