Page 427 - ACFE Fraud Reports 2009_2020

P. 427

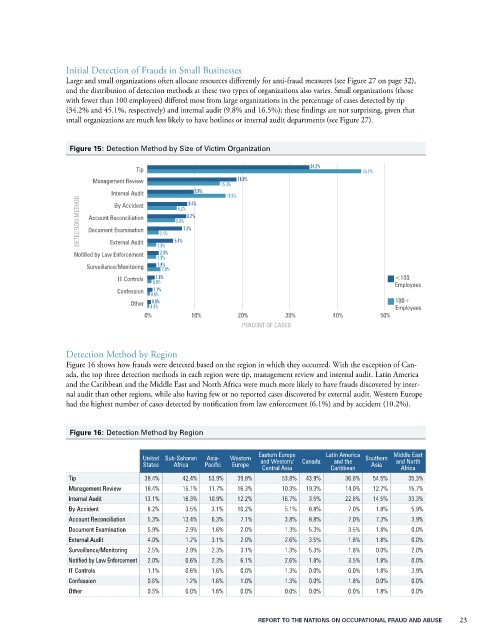

Initial Detection of Frauds in Small Businesses

Large and small organizations often allocate resources differently for anti-fraud measures (see Figure 27 on page 32),

and the distribution of detection methods at these two types of organizations also varies. Small organizations (those

with fewer than 100 employees) differed most from large organizations in the percentage of cases detected by tip

(34.2% and 45.1%, respectively) and internal audit (9.8% and 16.5%); these findings are not surprising, given that

small organizations are much less likely to have hotlines or internal audit departments (see Figure 27).

Figure 15: Detection Method by Size of Victim Organization

34.2%

Tip 45.1%

Management Review 18.8%

15.3%

Internal Audit 8.4% 9.8% 16.5%

DETECTION METHOD Document Examination 2.4% 5.9% 7.3% 8.2%

By Accident

6.2%

Account Reconciliation

External Audit

2.4%

Notified by Law Enforcement 1.9% 5.4%

1.9%

Surveillance/Monitoring 1.9% 2.8%

1.6%

IT Controls 0.9% <100

1.1%

Confession 0.6% Employees

0.8%

Other 0.4% 100+

Employees

0% 10% 20% 30% 40% 50%

PERCENT OF CASES

Detection Method by Region

Figure 16 shows how frauds were detected based on the region in which they occurred. With the exception of Can-

ada, the top three detection methods in each region were tip, management review and internal audit. Latin America

and the Caribbean and the Middle East and North Africa were much more likely to have frauds discovered by inter-

nal audit than other regions, while also having few or no reported cases discovered by external audit. Western Europe

had the highest number of cases detected by notification from law enforcement (6.1%) and by accident (10.2%).

Figure 16: Detection Method by Region

United Sub-Saharan Asia- Western Eastern Europe Canada Latin America Southern Middle East

and North

and Western/

and the

States Africa Pacific Europe Central Asia Caribbean Asia Africa

Tip 38.4% 42.4% 53.9% 39.8% 53.8% 43.9% 36.8% 54.5% 35.3%

Management Review 18.4% 15.1% 11.7% 16.3% 10.3% 19.3% 14.0% 12.7% 15.7%

Internal Audit 13.1% 16.3% 10.9% 12.2% 16.7% 3.5% 22.8% 14.5% 33.3%

By Accident 8.2% 3.5% 3.1% 10.2% 5.1% 8.8% 7.0% 1.8% 5.9%

Account Reconciliation 5.3% 13.4% 6.3% 7.1% 3.8% 8.8% 7.0% 7.3% 3.9%

Document Examination 5.9% 2.9% 1.6% 2.0% 1.3% 5.3% 3.5% 1.8% 0.0%

External Audit 4.0% 1.2% 3.1% 2.0% 2.6% 3.5% 1.8% 1.8% 0.0%

Surveillance/Monitoring 2.5% 2.9% 2.3% 3.1% 1.3% 5.3% 1.8% 0.0% 2.0%

Notified by Law Enforcement 2.0% 0.6% 2.3% 6.1% 2.6% 1.8% 3.5% 1.8% 0.0%

IT Controls 1.1% 0.6% 1.6% 0.0% 1.3% 0.0% 0.0% 1.8% 3.9%

Confession 0.6% 1.2% 1.6% 1.0% 1.3% 0.0% 1.8% 0.0% 0.0%

Other 0.5% 0.0% 1.6% 0.0% 0.0% 0.0% 0.0% 1.8% 0.0%

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 23