Page 465 - ACFE Fraud Reports 2009_2020

P. 465

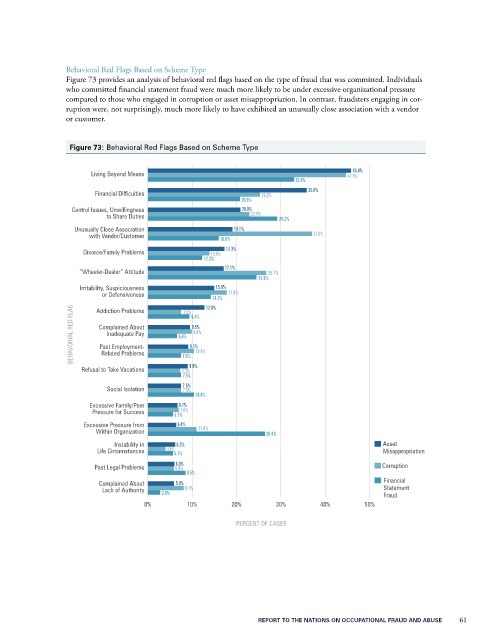

Behavioral Red Flags Based on Scheme Type

Figure 73 provides an analysis of behavioral red flags based on the type of fraud that was committed. Individuals

who committed financial statement fraud were much more likely to be under excessive organizational pressure

compared to those who engaged in corruption or asset misappropriation. In contrast, fraudsters engaging in cor-

ruption were, not surprisingly, much more likely to have exhibited an unusually close association with a vendor

or customer.

Figure 73: Behavioral Red Flags Based on Scheme Type

45.8%

Living Beyond Means 44.7%

33.0%

35.8%

Financial Difficulties 25.3%

20.8%

Control Issues, Unwillingness 20.9%

to Share Duties 22.9% 29.2%

Unusually Close Association 19.1%

with Vendor/Customer 37.0%

16.0%

17.3%

Divorce/Family Problems 13.9%

12.3%

17.1%

“Wheeler-Dealer” Attitude 26.7%

24.5%

Irritability, Suspiciousness 15.0%

or Defensiveness 17.8%

14.2%

12.8%

BEHAVORIAL RED FLAG Complained About 6.6% 9.1% 10.4%

Addiction Problems

7.5%

9.4%

9.5%

9.9%

Inadequate Pay

Past Employment-

Related Problems

7.5%

Refusal to Take Vacations 7.3% 9.0%

7.5%

Social Isolation 7.5%

7.5%

10.4%

Excessive Family/Peer 6.7%

Pressure for Success 5.7% 7.0%

Excessive Pressure from 6.4% 11.0%

Within Organization 26.4%

Instability in 6.2% Asset

Life Circumstances 4.0% 5.7% Misappropriation

6.0%

Past Legal Problems 5.9% Corruption

8.5%

Financial

Complained About 5.9%

Lack of Authority 2.8% 8.1% Statement

Fraud

0% 10% 20% 30% 40% 50%

PERCENT OF CASES

REPORT TO THE NATIONS ON OCCUPATIONAL FRAUD AND ABUSE 61