Page 645 - ACFE Fraud Reports 2009_2020

P. 645

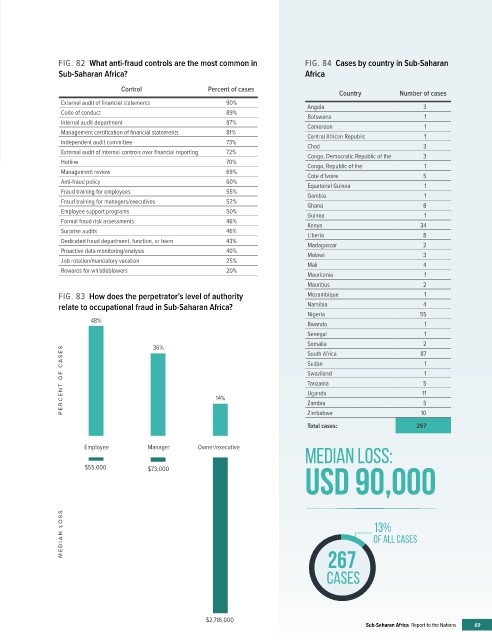

FIG. 82 What anti-fraud controls are the most common in FIG. 84 Cases by country in Sub-Saharan

Sub-Saharan Africa? Africa

Control Percent of cases

Country Number of cases

External audit of financial statements 90%

Angola 3

Code of conduct 89%

Botswana 1

Internal audit department 87%

Cameroon 1

Management certification of financial statements 81% Central African Republic 1

Independent audit committee 73% Chad 3

External audit of internal controls over financial reporting 72% Congo, Democratic Republic of the 3

Hotline 70% Congo, Republic of the 1

Management review 69% Cote d’Ivoire 5

Anti-fraud policy 60% Equatorial Guinea 1

Fraud training for employees 55%

Gambia 1

Fraud training for managers/executives 52%

Ghana 8

Employee support programs 50%

Guinea 1

Formal fraud risk assessments 46%

Kenya 34

Surprise audits 46%

Liberia 8

Dedicated fraud department, function, or team 43%

Madagascar 2

Proactive data monitoring/analysis 40%

Malawi 3

Job rotation/mandatory vacation 25% Mali 4

Rewards for whistleblowers 20%

Mauritania 1

Mauritius 2

FIG. 83 How does the perpetrator’s level of authority Mozambique 1

relate to occupational fraud in Sub-Saharan Africa? Namibia 4

Nigeria 55

48%

Rwanda 1

Senegal 1

Somalia 2

36% South Africa 87 1

PERCENT OF C A SES 14% Swaziland 11 5 5 1

Sudan

Tanzania

Uganda

Zambia

Zimbabwe

10

Total cases: 267

Employee Manager Owner/executive

MEDIAN LOSS:

usd 90,000

$55,000 $73,000

� � � � �

MEDIAN L OSS 13%

OF ALL CASES

267

CASES

$2,716,000

Sub-Saharan Africa Report to the Nations 69