Page 740 - ACFE Fraud Reports 2009_2020

P. 740

FRAUD PREVENTION

CHECKLIST

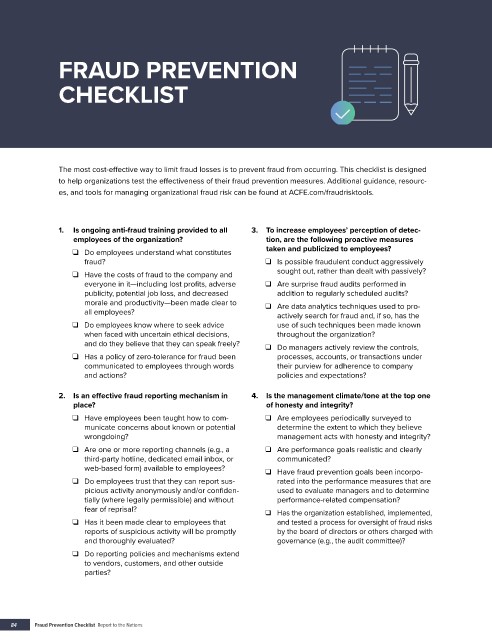

The most cost-effective way to limit fraud losses is to prevent fraud from occurring. This checklist is designed

to help organizations test the effectiveness of their fraud prevention measures. Additional guidance, resourc-

es, and tools for managing organizational fraud risk can be found at ACFE.com/fraudrisktools.

1. Is ongoing anti-fraud training provided to all 3. To increase employees’ perception of detec-

employees of the organization? tion, are the following proactive measures

❑ Do employees understand what constitutes taken and publicized to employees?

fraud? ❑ Is possible fraudulent conduct aggressively

❑ Have the costs of fraud to the company and sought out, rather than dealt with passively?

everyone in it—including lost profits, adverse ❑ Are surprise fraud audits performed in

publicity, potential job loss, and decreased addition to regularly scheduled audits?

morale and productivity—been made clear to ❑ Are data analytics techniques used to pro-

all employees? actively search for fraud and, if so, has the

❑ Do employees know where to seek advice use of such techniques been made known

when faced with uncertain ethical decisions, throughout the organization?

and do they believe that they can speak freely?

❑ Do managers actively review the controls,

❑ Has a policy of zero-tolerance for fraud been processes, accounts, or transactions under

communicated to employees through words their purview for adherence to company

and actions? policies and expectations?

2. Is an effective fraud reporting mechanism in 4. Is the management climate/tone at the top one

place? of honesty and integrity?

❑ Have employees been taught how to com- ❑ Are employees periodically surveyed to

municate concerns about known or potential determine the extent to which they believe

wrongdoing? management acts with honesty and integrity?

❑ Are one or more reporting channels (e.g., a ❑ Are performance goals realistic and clearly

third-party hotline, dedicated email inbox, or communicated?

web-based form) available to employees?

❑ Have fraud prevention goals been incorpo-

❑ Do employees trust that they can report sus- rated into the performance measures that are

picious activity anonymously and/or confiden- used to evaluate managers and to determine

tially (where legally permissible) and without performance-related compensation?

fear of reprisal? ❑ Has the organization established, implemented,

❑ Has it been made clear to employees that and tested a process for oversight of fraud risks

reports of suspicious activity will be promptly by the board of directors or others charged with

and thoroughly evaluated? governance (e.g., the audit committee)?

❑ Do reporting policies and mechanisms extend

to vendors, customers, and other outside

parties?

84 Fraud Prevention Checklist Report to the Nations