Page 33 - Banking Finance March 2023

P. 33

ARTICLE

favourable digital ecosystem for the development of digital The smart phone revolution

lending. India has pioneered in creating conducive ecosystem

Big data analytics, Artificial Intelligence (AI) and

for development of Fin-Techs and digital transactions.

Machine Learning (ML)

Enabling technological developments

The digital lending ecosystem has myriad levels of

complexity and is in a constant state of evolution. Digital Eco-system conducive for digital lenders and Fin-Tech

lending is the process of offering loans that are applied for, companies

disbursed, and managed through digital channels. In this

Increased digital uptake to overcome challenges posed

process, lenders use digitised data to make credit decisions

by COVID-19

and build intelligent customer engagement (Accion, 2018).

Digital Lending

Landscape

The Indian Digital Lending

landscape has undergone

a dramatic shift over the

past few years. The

legacy systems and

traditional practices that

were prominent in this

space are disappearing

and getting replaced

with digital processes that

are powered by data and

AI. This transformation

has been further

accelerated by COVID-19

(RBI Report 2021) and the social distancing norms put to counter it.

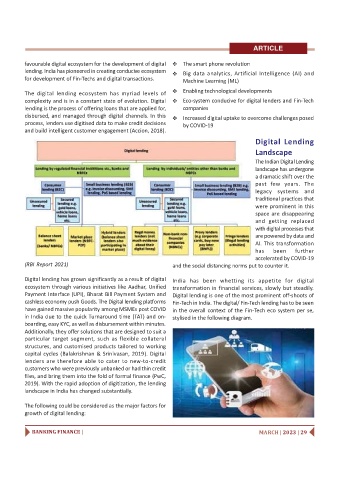

Digital lending has grown significantly as a result of digital India has been whetting its appetite for digital

ecosystem through various initiatives like Aadhar, Unified transformation in financial services, slowly but steadily.

Payment Interface (UPI), Bharat Bill Payment System and Digital lending is one of the most prominent off-shoots of

cashless economy push Goods. The Digital lending platforms Fin-Tech in India. The digital/ Fin-Tech lending has to be seen

have gained massive popularity among MSMEs post COVID in the overall context of the Fin-Tech eco system per se,

in India due to the quick Turnaround time (TAT) and on- stylised in the following diagram.

boarding, easy KYC, as well as disbursement within minutes.

Additionally, they offer solutions that are designed to suit a

particular target segment, such as flexible collateral

structures, and customised products tailored to working

capital cycles (Balakrishnan & Srinivasan, 2019). Digital

lenders are therefore able to cater to new-to-credit

customers who were previously unbanked or had thin credit

files, and bring them into the fold of formal finance (PwC,

2019). With the rapid adoption of digitization, the lending

landscape in India has changed substantially.

The following could be considered as the major factors for

growth of digital lending:

BANKING FINANCE | MARCH | 2023 | 29