Page 282 - Ebook health insurance IC27

P. 282

The Insurance Times

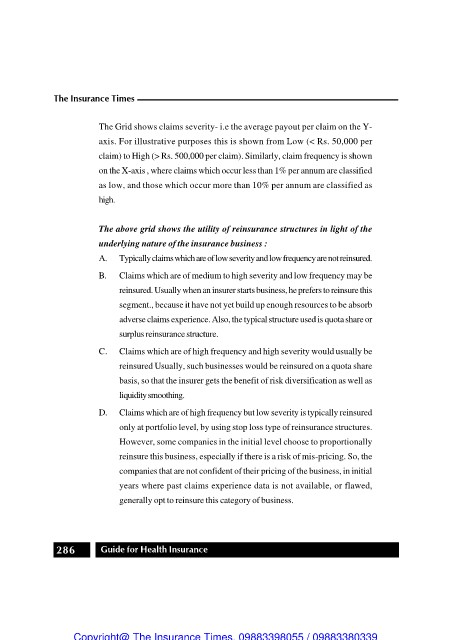

The Grid shows claims severity- i.e the average payout per claim on the Y-

axis. For illustrative purposes this is shown from Low (< Rs. 50,000 per

claim) to High (> Rs. 500,000 per claim). Similarly, claim frequency is shown

on the X-axis , where claims which occur less than 1% per annum are classified

as low, and those which occur more than 10% per annum are classified as

high.

The above grid shows the utility of reinsurance structures in light of the

underlying nature of the insurance business :

A. Typically claimswhich are oflowseverity and lowfrequencyarenot reinsured.

B. Claims which are of medium to high severity and low frequency may be

reinsured. Usually when an insurer starts business, he prefers to reinsure this

segment., because it have not yet build up enough resources to be absorb

adverse claims experience. Also, the typical structure used is quota share or

surplus reinsurance structure.

C. Claims which are of high frequency and high severity would usually be

reinsured Usually, such businesses would be reinsured on a quota share

basis, so that the insurer gets the benefit of risk diversification as well as

liquidity smoothing.

D. Claims which are of high frequency but low severity is typically reinsured

only at portfolio level, by using stop loss type of reinsurance structures.

However, some companies in the initial level choose to proportionally

reinsure this business, especially if there is a risk of mis-pricing. So, the

companies that are not confident of their pricing of the business, in initial

years where past claims experience data is not available, or flawed,

generally opt to reinsure this category of business.

286 Guide for Health Insurance