Page 4 - BE Theory Note

P. 4

Contribution

The first thing you need to be able to do is to calculate the contribution

When you have calculated the fixed costs, you need to make sure that they are

covered before you can make a profit

Every time you sell a product, you can work out the “mini profit” on each by

subtracting the variable cost from the selling price. For example, with a selling

price of £10 and a variable cost of £5, you are making a £5 profit on each product.

Each of these £5 “mini profits” needs to go towards the fixed costs and ONCE the

fixed costs are covered, then the business will start making a profit.

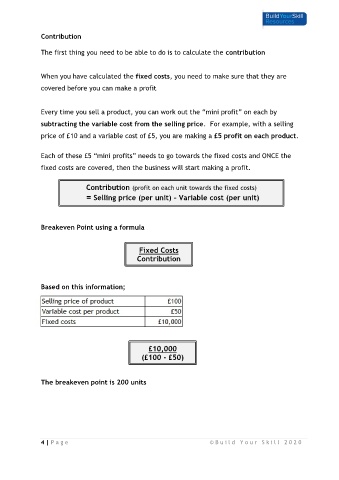

Contribution (profit on each unit towards the fixed costs)

= Selling price (per unit) – Variable cost (per unit)

Breakeven Point using a formula

Fixed Costs

Contribution

Based on this information;

£10,000

(£100 - £50)

The breakeven point is 200 units

4 | P a g e © B u i l d Y o u r S k i l l 2 0 2 0