Page 48 - pwc-lease-accounting-guide_Neat

P. 48

Scope

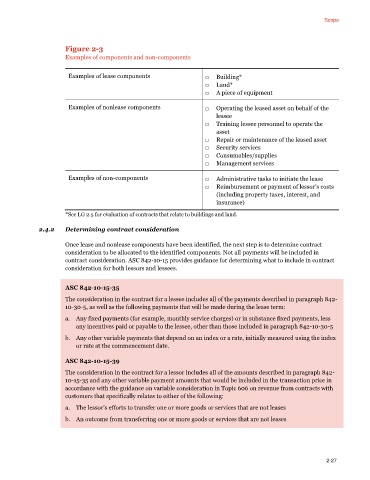

Figure 2-3

Examples of components and non-components

Examples of lease components □ Building*

□ Land*

□ A piece of equipment

Examples of nonlease components □ Operating the leased asset on behalf of the

lessee

□ Training lessee personnel to operate the

asset

□ Repair or maintenance of the leased asset

□ Security services

□ Consumables/supplies

□ Management services

Examples of non-components □ Administrative tasks to initiate the lease

□ Reimbursement or payment of lessor’s costs

(including property taxes, interest, and

insurance)

*See LG 2.5 for evaluation of contracts that relate to buildings and land.

2.4.2 Determining contract consideration

Once lease and nonlease components have been identified, the next step is to determine contract

consideration to be allocated to the identified components. Not all payments will be included in

contract consideration. ASC 842-10-15 provides guidance for determining what to include in contract

consideration for both lessors and lessees.

ASC 842-10-15-35

The consideration in the contract for a lessee includes all of the payments described in paragraph 842-

10-30-5, as well as the following payments that will be made during the lease term:

a. Any fixed payments (for example, monthly service charges) or in substance fixed payments, less

any incentives paid or payable to the lessee, other than those included in paragraph 842-10-30-5

b. Any other variable payments that depend on an index or a rate, initially measured using the index

or rate at the commencement date.

ASC 842-10-15-39

The consideration in the contract for a lessor includes all of the amounts described in paragraph 842-

10-15-35 and any other variable payment amounts that would be included in the transaction price in

accordance with the guidance on variable consideration in Topic 606 on revenue from contracts with

customers that specifically relates to either of the following:

a. The lessor’s efforts to transfer one or more goods or services that are not leases

b. An outcome from transferring one or more goods or services that are not leases

2-27