Page 49 - pwc-lease-accounting-guide_Neat

P. 49

Scope

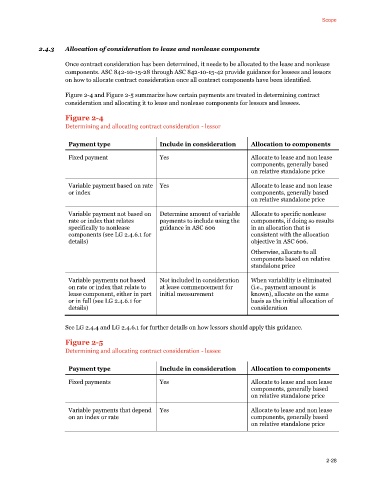

2.4.3 Allocation of consideration to lease and nonlease components

Once contract consideration has been determined, it needs to be allocated to the lease and nonlease

components. ASC 842-10-15-28 through ASC 842-10-15-42 provide guidance for lessees and lessors

on how to allocate contract consideration once all contract components have been identified.

Figure 2-4 and Figure 2-5 summarize how certain payments are treated in determining contract

consideration and allocating it to lease and nonlease components for lessors and lessees.

Figure 2-4

Determining and allocating contract consideration - lessor

Payment type Include in consideration Allocation to components

Fixed payment Yes Allocate to lease and non lease

components, generally based

on relative standalone price

Variable payment based on rate Yes Allocate to lease and non lease

or index components, generally based

on relative standalone price

Variable payment not based on Determine amount of variable Allocate to specific nonlease

rate or index that relates payments to include using the components, if doing so results

specifically to nonlease guidance in ASC 606 in an allocation that is

components (see LG 2.4.6.1 for consistent with the allocation

details) objective in ASC 606.

Otherwise, allocate to all

components based on relative

standalone price

Variable payments not based Not included in consideration When variability is eliminated

on rate or index that relate to at lease commencement for (i.e., payment amount is

lease component, either in part initial measurement known), allocate on the same

or in full (see LG 2.4.6.1 for basis as the initial allocation of

details) consideration

See LG 2.4.4 and LG 2.4.6.1 for further details on how lessors should apply this guidance.

Figure 2-5

Determining and allocating contract consideration - lessee

Payment type Include in consideration Allocation to components

Fixed payments Yes Allocate to lease and non lease

components, generally based

on relative standalone price

Variable payments that depend Yes Allocate to lease and non lease

on an index or rate components, generally based

on relative standalone price

2-28