Page 53 - pwc-lease-accounting-guide_Neat

P. 53

Scope

guidance, and the amount of variable payments allocated to nonlease components would be

recognized in accordance with other guidance, such as the revenue recognition guidance.

As of the cut-off date of this guide, the proposed amendments have not yet been issued. Reporting

entities should continue to monitor the status of these proposed amendments and any additional

updates to the new leases guidance. The variable payment accounting model described within this

chapter is based on the guidance in ASC 842-10-15-40 as currently written.

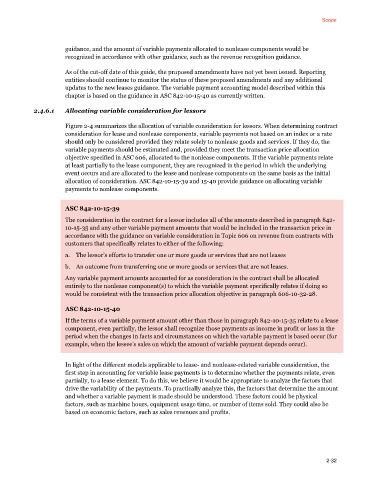

2.4.6.1 Allocating variable consideration for lessors

Figure 2-4 summarizes the allocation of variable consideration for lessors. When determining contract

consideration for lease and nonlease components, variable payments not based on an index or a rate

should only be considered provided they relate solely to nonlease goods and services. If they do, the

variable payments should be estimated and, provided they meet the transaction price allocation

objective specified in ASC 606, allocated to the nonlease components. If the variable payments relate

at least partially to the lease component, they are recognized in the period in which the underlying

event occurs and are allocated to the lease and nonlease components on the same basis as the initial

allocation of consideration. ASC 842-10-15-39 and 15-40 provide guidance on allocating variable

payments to nonlease components.

ASC 842-10-15-39

The consideration in the contract for a lessor includes all of the amounts described in paragraph 842-

10-15-35 and any other variable payment amounts that would be included in the transaction price in

accordance with the guidance on variable consideration in Topic 606 on revenue from contracts with

customers that specifically relates to either of the following:

a. The lessor’s efforts to transfer one or more goods or services that are not leases

b. An outcome from transferring one or more goods or services that are not leases.

Any variable payment amounts accounted for as consideration in the contract shall be allocated

entirely to the nonlease component(s) to which the variable payment specifically relates if doing so

would be consistent with the transaction price allocation objective in paragraph 606-10-32-28.

ASC 842-10-15-40

If the terms of a variable payment amount other than those in paragraph 842-10-15-35 relate to a lease

component, even partially, the lessor shall recognize those payments as income in profit or loss in the

period when the changes in facts and circumstances on which the variable payment is based occur (for

example, when the lessee’s sales on which the amount of variable payment depends occur).

In light of the different models applicable to lease- and nonlease-related variable consideration, the

first step in accounting for variable lease payments is to determine whether the payments relate, even

partially, to a lease element. To do this, we believe it would be appropriate to analyze the factors that

drive the variability of the payments. To practically analyze this, the factors that determine the amount

and whether a variable payment is made should be understood. These factors could be physical

factors, such as machine hours, equipment usage time, or number of items sold. They could also be

based on economic factors, such as sales revenues and profits.

2-32