Page 57 - pwc-lease-accounting-guide_Neat

P. 57

Scope

believes that it will be entitled to at least part of the variable payments regardless of whether the

consulting services are provided. Therefore, the variable payments relate, at least partially, to the lease

component. Consequently, the variable consideration should be excluded from the allocation of

consideration used for initial measurement, and will be allocated to both the lease and nonlease

components when the underlying event occurs.

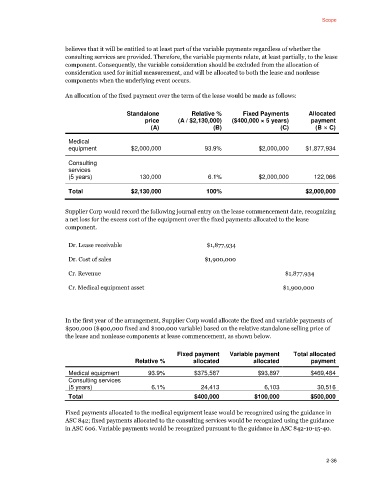

An allocation of the fixed payment over the term of the lease would be made as follows:

Standalone Relative % Fixed Payments Allocated

price (A / $2,130,000) ($400,000 × 5 years) payment

(A) (B) (C) (B × C)

Medical

equipment $2,000,000 93.9% $2,000,000 $1,877,934

Consulting

services

(5 years) 130,000 6.1% $2,000,000 122,066

Total $2,130,000 100% $2,000,000

Supplier Corp would record the following journal entry on the lease commencement date, recognizing

a net loss for the excess cost of the equipment over the fixed payments allocated to the lease

component.

Dr. Lease receivable $1,877,934

Dr. Cost of sales $1,900,000

Cr. Revenue $1,877,934

Cr. Medical equipment asset $1,900,000

In the first year of the arrangement, Supplier Corp would allocate the fixed and variable payments of

$500,000 ($400,000 fixed and $100,000 variable) based on the relative standalone selling price of

the lease and nonlease components at lease commencement, as shown below.

Fixed payment Variable payment Total allocated

Relative % allocated allocated payment

Medical equipment 93.9% $375,587 $93,897 $469,484

Consulting services

(5 years) 6.1% 24,413 6,103 30,516

Total $400,000 $100,000 $500,000

Fixed payments allocated to the medical equipment lease would be recognized using the guidance in

ASC 842; fixed payments allocated to the consulting services would be recognized using the guidance

in ASC 606. Variable payments would be recognized pursuant to the guidance in ASC 842-10-15-40.

2-36