Page 59 - pwc-lease-accounting-guide_Neat

P. 59

Scope

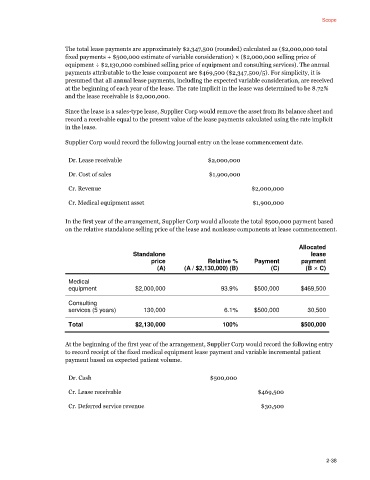

The total lease payments are approximately $2,347,500 (rounded) calculated as ($2,000,000 total

fixed payments + $500,000 estimate of variable consideration) × ($2,000,000 selling price of

equipment ÷ $2,130,000 combined selling price of equipment and consulting services). The annual

payments attributable to the lease component are $469,500 ($2,347,500/5). For simplicity, it is

presumed that all annual lease payments, including the expected variable consideration, are received

at the beginning of each year of the lease. The rate implicit in the lease was determined to be 8.72%

and the lease receivable is $2,000,000.

Since the lease is a sales-type lease, Supplier Corp would remove the asset from its balance sheet and

record a receivable equal to the present value of the lease payments calculated using the rate implicit

in the lease.

Supplier Corp would record the following journal entry on the lease commencement date.

Dr. Lease receivable $2,000,000

Dr. Cost of sales $1,900,000

Cr. Revenue $2,000,000

Cr. Medical equipment asset $1,900,000

In the first year of the arrangement, Supplier Corp would allocate the total $500,000 payment based

on the relative standalone selling price of the lease and nonlease components at lease commencement.

Allocated

Standalone lease

price Relative % Payment payment

(A) (A / $2,130,000) (B) (C) (B × C)

Medical

equipment $2,000,000 93.9% $500,000 $469,500

Consulting

services (5 years) 130,000 6.1% $500,000 30,500

Total $2,130,000 100% $500,000

At the beginning of the first year of the arrangement, Supplier Corp would record the following entry

to record receipt of the fixed medical equipment lease payment and variable incremental patient

payment based on expected patient volume.

Dr. Cash $500,000

Cr. Lease receivable $469,500

Cr. Deferred service revenue $30,500

2-38