Page 61 - pwc-lease-accounting-guide_Neat

P. 61

Scope

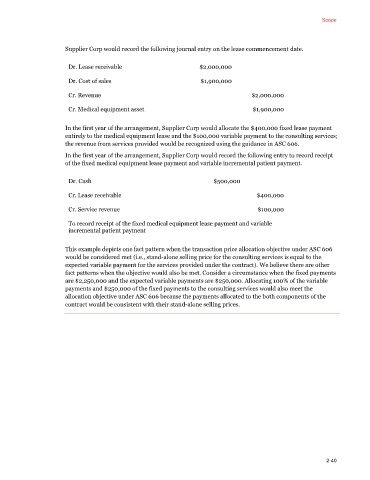

Supplier Corp would record the following journal entry on the lease commencement date.

Dr. Lease receivable $2,000,000

Dr. Cost of sales $1,900,000

Cr. Revenue $2,000,000

Cr. Medical equipment asset $1,900,000

In the first year of the arrangement, Supplier Corp would allocate the $400,000 fixed lease payment

entirely to the medical equipment lease and the $100,000 variable payment to the consulting services;

the revenue from services provided would be recognized using the guidance in ASC 606.

In the first year of the arrangement, Supplier Corp would record the following entry to record receipt

of the fixed medical equipment lease payment and variable incremental patient payment.

Dr. Cash $500,000

Cr. Lease receivable $400,000

Cr. Service revenue $100,000

To record receipt of the fixed medical equipment lease payment and variable

incremental patient payment

This example depicts one fact pattern when the transaction price allocation objective under ASC 606

would be considered met (i.e., stand-alone selling price for the consulting services is equal to the

expected variable payment for the services provided under the contract). We believe there are other

fact patterns when the objective would also be met. Consider a circumstance when the fixed payments

are $2,250,000 and the expected variable payments are $250,000. Allocating 100% of the variable

payments and $250,000 of the fixed payments to the consulting services would also meet the

allocation objective under ASC 606 because the payments allocated to the both components of the

contract would be consistent with their stand-alone selling prices.

2-40