Page 62 - pwc-lease-accounting-guide_Neat

P. 62

Scope

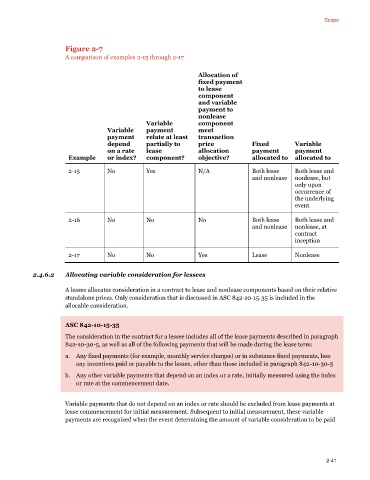

Figure 2-7

A comparison of examples 2-15 through 2-17

Allocation of

fixed payment

to lease

component

and variable

payment to

nonlease

Variable component

Variable payment meet

payment relate at least transaction

depend partially to price Fixed Variable

on a rate lease allocation payment payment

Example or index? component? objective? allocated to allocated to

2-15 No Yes N/A Both lease Both lease and

and nonlease nonlease, but

only upon

occurrence of

the underlying

event

2-16 No No No Both lease Both lease and

and nonlease nonlease, at

contract

inception

2-17 No No Yes Lease Nonlease

2.4.6.2 Allocating variable consideration for lessees

A lessee allocates consideration in a contract to lease and nonlease components based on their relative

standalone prices. Only consideration that is discussed in ASC 842-10-15-35 is included in the

allocable consideration.

ASC 842-10-15-35

The consideration in the contract for a lessee includes all of the lease payments described in paragraph

842-10-30-5, as well as all of the following payments that will be made during the lease term:

a. Any fixed payments (for example, monthly service charges) or in substance fixed payments, less

any incentives paid or payable to the lessee, other than those included in paragraph 842-10-30-5

b. Any other variable payments that depend on an index or a rate, initially measured using the index

or rate at the commencement date.

Variable payments that do not depend on an index or rate should be excluded from lease payments at

lease commencement for initial measurement. Subsequent to initial measurement, these variable

payments are recognized when the event determining the amount of variable consideration to be paid

2-41