Page 58 - pwc-lease-accounting-guide_Neat

P. 58

Scope

During the first year of the arrangement, Supplier Corp would record the following journal entry:

Dr. Cash $500,000

Cr. Lease receivable $375,587

Cr. Lease revenue $93,897

Cr. Service revenue $30,516

EXAMPLE 2-16

Allocating variable consideration – contract for sale of medical equipment and consulting services

(sales-type lease)

Assume the same facts as Example 2-15 except that while the new equipment will provide better

patient care, it is not expected to significantly impact the number of patients that Customer Co can

treat. Increases in the number of patients Customer Co can treat will result primarily from the

optimization of processes as a result of the consulting services. Absent those services, it is unlikely that

the 6,000 patient threshold would be met.

How should Supplier Corp account for this arrangement at lease commencement and in the first year?

Analysis

The equipment lease and consulting services are separate lease and nonlease components,

respectively. The variable payments relate specifically to the nonlease component.

In this example, we are assuming that Supplier Corp allocates the variable payments to the lease and

nonlease components based on relative standalone selling price, as the transaction price allocation

objective is not met. However, if a lessor believes that allocating the variable consideration entirely to

the nonlease component is consistent with the transaction price allocation objective in ASC 606-10-

32-28, then it should do so, as demonstrated in Example 2-17. See RR 5 for information on allocating

variable consideration.

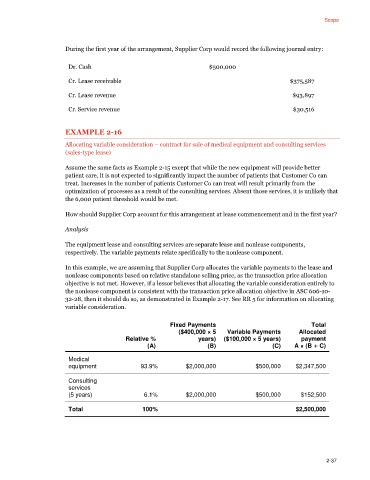

Fixed Payments Total

($400,000 × 5 Variable Payments Allocated

Relative % years) ($100,000 × 5 years) payment

(A) (B) (C) A × (B + C)

Medical

equipment 93.9% $2,000,000 $500,000 $2,347,500

Consulting

services

(5 years) 6.1% $2,000,000 $500,000 $152,500

Total 100% $2,500,000

2-37