Page 344 - Accounting Principles (A Business Perspective)

P. 344

8. Control of cash

DEPOSIT 1,000.00 2010/09/28 4,310.88

NEF CHECK 102.00 2010/09/30 4,208.88

SERVICE CHARGE 8,00 2010/09/30 4,200.88

SAFE DEPOSIT BOX REMT 15.00 2010/09/30 4,185.38

BALANCE THIS STATEMENT 2010/09/30 4,1S5.3S

TOTAL CREDITS (2) S,300.00 MINIMUM BALANCE 3,195.68

TOTAL DEBITS (7) 7,708.55 AVG AVAILABLE BALAHCE 5,236.31

Average BALANCE 5,23S,31

YOUR CHECKS

SEQUENCED

DATE CHECK # AMOUNT DATE CHECK # AMOUNT DATE CHECK # AMOUNT

1031* 102.41 09/18 1036 38.95 03/25 1039 137,45

09/08 1033* 6B. 77 09/20 1037 16.08

09/21 1035 114.90 09/21 1033 7,105,00

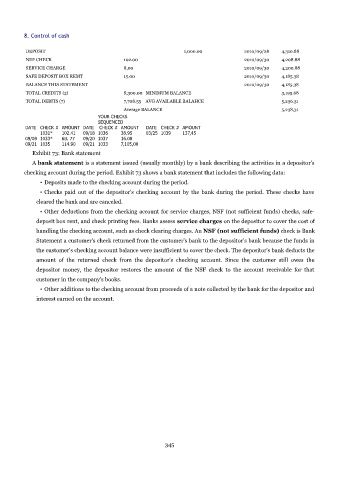

Exhibit 73: Bank statement

A bank statement is a statement issued (usually monthly) by a bank describing the activities in a depositor's

checking account during the period. Exhibit 73 shows a bank statement that includes the following data:

• Deposits made to the checking account during the period.

• Checks paid out of the depositor's checking account by the bank during the period. These checks have

cleared the bank and are canceled.

• Other deductions from the checking account for service charges, NSF (not sufficient funds) checks, safe-

deposit box rent, and check printing fees. Banks assess service charges on the depositor to cover the cost of

handling the checking account, such as check clearing charges. An NSF (not sufficient funds) check is Bank

Statement a customer's check returned from the customer's bank to the depositor's bank because the funds in

the customer's checking account balance were insufficient to cover the check. The depositor's bank deducts the

amount of the returned check from the depositor's checking account. Since the customer still owes the

depositor money, the depositor restores the amount of the NSF check to the account receivable for that

customer in the company's books.

• Other additions to the checking account from proceeds of a note collected by the bank for the depositor and

interest earned on the account.

345