Page 45 - NCCAA Finance Board Accountability

P. 45

Ratios

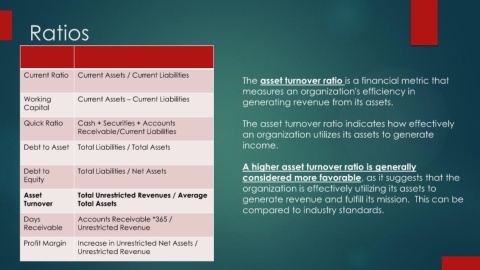

Current Ratio Current Assets / Current Liabilities

The asset turnover ratio is a financial metric that

measures an organization's efficiency in

Working Current Assets – Current Liabilities generating revenue from its assets.

Capital

Quick Ratio Cash + Securities + Accounts The asset turnover ratio indicates how effectively

Receivable/Current Liabilities an organization utilizes its assets to generate

Debt to Asset Total Liabilities / Total Assets income.

A higher asset turnover ratio is generally

Debt to Total Liabilities / Net Assets

Equity considered more favorable, as it suggests that the

organization is effectively utilizing its assets to

Asset Total Unrestricted Revenues / Average generate revenue and fulfill its mission. This can be

Turnover Total Assets

compared to industry standards.

Days Accounts Receivable *365 /

Receivable Unrestricted Revenue

Profit Margin Increase in Unrestricted Net Assets /

Unrestricted Revenue