Page 147 - Internal Auditing Standards

P. 147

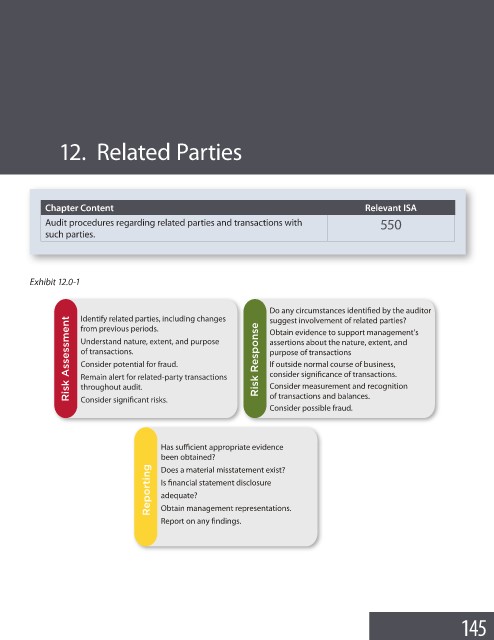

12. Related Parties

Chapter Content Relevant ISA

Audit procedures regarding related parties and transactions with 550

such parties.

Exhibit 12.0-1

Do any circumstances identified by the auditor

Identify related parties, including changes

@WaY /aaSaa[S\b Understand nature, extent, and purpose @WaY @Sa^]\aS assertions about the nature, extent, and

suggest involvement of related parties?

from previous periods.

Obtain evidence to support management’s

of transactions.

purpose of transactions

If outside normal course of business,

Consider potential for fraud.

consider significance of transactions.

Remain alert for related-party transactions

Consider measurement and recognition

throughout audit.

of transactions and balances.

Consider significant risks.

Consider possible fraud.

Has sufficient appropriate evidence

been obtained?

@S^]`bW\U Is financial statement disclosure

Does a material misstatement exist?

adequate?

Obtain management representations.

Report on any findings.

145