Page 142 - Internal Auditing Standards

P. 142

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

CONSIDER POINT

Where the use of a management expert would greatly assist the estimating process, discuss this need

with entity management as early as possible in the audit process so that appropriate action can be

taken.

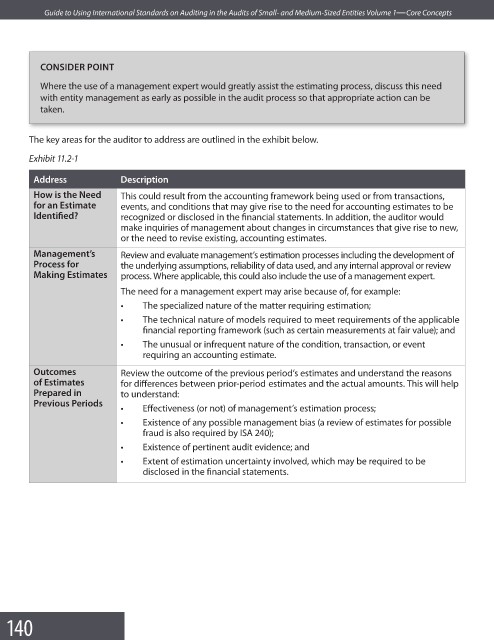

The key areas for the auditor to address are outlined in the exhibit below.

Exhibit 11.2-1

Address Description

How is the Need This could result from the accounting framework being used or from transactions,

for an Estimate events, and conditions that may give rise to the need for accounting estimates to be

Identifi ed? recognized or disclosed in the financial statements. In addition, the auditor would

make inquiries of management about changes in circumstances that give rise to new,

or the need to revise existing, accounting estimates.

Management’s Review and evaluate management’s estimation processes including the development of

Process for the underlying assumptions, reliability of data used, and any internal approval or review

Making Estimates process. Where applicable, this could also include the use of a management expert.

The need for a management expert may arise because of, for example:

• The specialized nature of the matter requiring estimation;

• The technical nature of models required to meet requirements of the applicable

financial reporting framework (such as certain measurements at fair value); and

• The unusual or infrequent nature of the condition, transaction, or event

requiring an accounting estimate.

Outcomes Review the outcome of the previous period’s estimates and understand the reasons

of Estimates for differences between prior-period estimates and the actual amounts. This will help

Prepared in to understand:

Previous Periods

• Effectiveness (or not) of management’s estimation process;

• Existence of any possible management bias (a review of estimates for possible

fraud is also required by ISA 240);

• Existence of pertinent audit evidence; and

• Extent of estimation uncertainty involved, which may be required to be

disclosed in the fi nancial statements.

140