Page 138 - Internal Auditing Standards

P. 138

11. Accounting Estimates

Chapter Content Relevant ISAs

Audit procedures relating to the audit of accounting estimates, 540

including fair value accounting estimates and related disclosures in an

audit of fi nancial statements.

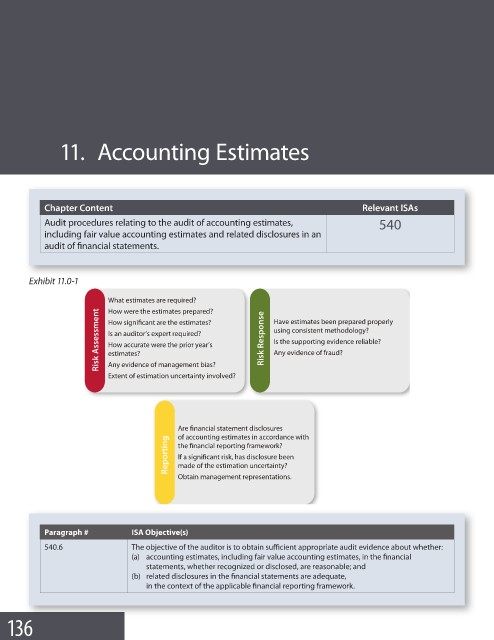

Exhibit 11.0-1

What estimates are required?

How were the estimates prepared?

Risk Assessment How significant are the estimates? Risk Response Have estimates been prepared properly

using consistent methodology?

Is an auditor’s expert required?

Is the supporting evidence reliable?

How accurate were the prior year’s

Any evidence of fraud?

estimates?

Any evidence of management bias?

Extent of estimation uncertainty involved?

Are financial statement disclosures

of accounting estimates in accordance with

Reporting the financial reporting framework?

If a significant risk, has disclosure been

made of the estimation uncertainty?

Obtain management representations.

Paragraph # ISA Objective(s)

540.6 The objective of the auditor is to obtain sufficient appropriate audit evidence about whether:

(a) accounting estimates, including fair value accounting estimates, in the fi nancial

statements, whether recognized or disclosed, are reasonable; and

(b) related disclosures in the financial statements are adequate,

in the context of the applicable financial reporting framework.

136