Page 202 - Internal Auditing Standards

P. 202

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

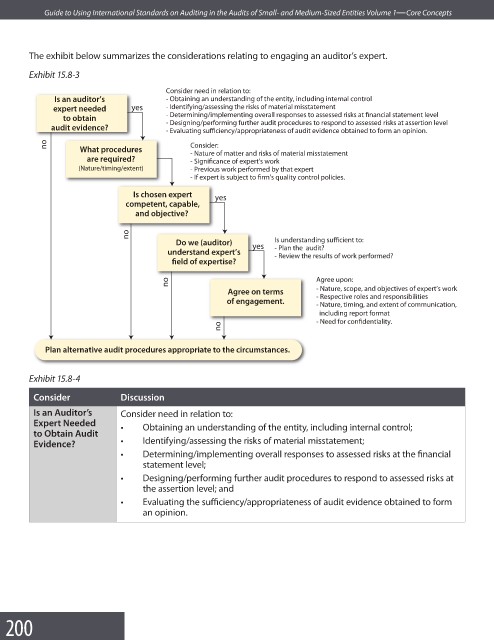

The exhibit below summarizes the considerations relating to engaging an auditor’s expert.

Exhibit 15.8-3

Consider need in relation to:

Is an auditor’s - Obtaining an understanding of the entity, including internal control

expert needed yes - Identifying/assessing the risks of material misstatement

to obtain - Determining/implementing overall responses to assessed risks at financial statement level

audit evidence? - Designing/performing further audit procedures to respond to assessed risks at assertion level

- Evaluating sufficiency/appropriateness of audit evidence obtained to form an opinion.

no Consider:

What procedures

- Nature of matter and risks of material misstatement

are required? - Significance of expert's work

(Nature/timing/extent) - Previous work performed by that expert

- If expert is subject to firm's quality control policies.

Is chosen expert yes

competent, capable,

and objective?

no

Do we (auditor) yes Is understanding sufficient to:

understand expert’s - Plan the audit?

- Review the results of work performed?

field of expertise?

no Agree upon:

Agree on terms - Nature, scope, and objectives of expert’s work

- Respective roles and responsibilities

of engagement.

- Nature, timing, and extent of communication,

including report format

- Need for confidentiality.

no

Plan alternative audit procedures appropriate to the circumstances.

Exhibit 15.8-4

Consider Discussion

Is an Auditor’s Consider need in relation to:

Expert Needed • Obtaining an understanding of the entity, including internal control;

to Obtain Audit

Evidence? • Identifying/assessing the risks of material misstatement;

• Determining/implementing overall responses to assessed risks at the fi nancial

statement level;

• Designing/performing further audit procedures to respond to assessed risks at

the assertion level; and

• Evaluating the sufficiency/appropriateness of audit evidence obtained to form

an opinion.

200