Page 206 - Internal Auditing Standards

P. 206

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

Paragraph # Relevant Extracts from ISAs

720.14 If, on reading the other information for the purpose of identifying material inconsistencies, the

auditor becomes aware of an apparent material misstatement of fact, the auditor shall discuss

the matter with management. (Ref: Para. A10)

720.15 If, following such discussions, the auditor still considers that there is an apparent material

misstatement of fact, the auditor shall request management to consult with a qualifi ed third

party, such as the entity’s legal counsel, and the auditor shall consider the advice received.

720.16 If the auditor concludes that there is a material misstatement of fact in the other information

which management refuses to correct, the auditor shall notify those charged with governance,

unless all of those charged with governance are involved in managing the entity, of the auditor’s

concern regarding the other information and take any further appropriate action. (Ref: Para. A11)

Overview

Some entities, such as those with many stakeholders, will publish (on paper or electronically) an annual report

or attach some additional information to the audited financial statements. Where this occurs, the auditor has a

responsibility to read the other information to identify any information that could undermine the credibility of

the financial statements and the auditor’s report. Should such information be found, the auditor needs to take

appropriate steps to rectify the situation.

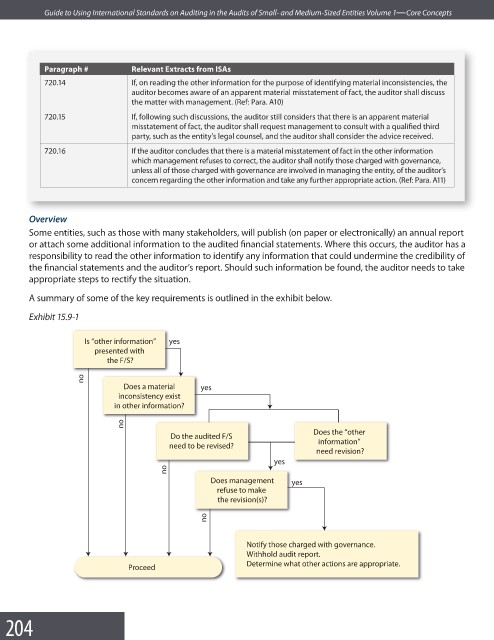

A summary of some of the key requirements is outlined in the exhibit below.

Exhibit 15.9-1

Is “other information” yes

presented with

the F/S?

no

Does a material yes

inconsistency exist

in other information?

no

Does the “other

Do the audited F/S

information”

need to be revised?

need revision?

yes

no

Does management yes

refuse to make

the revision(s)?

no

Notify those charged with governance.

Withhold audit report.

Determine what other actions are appropriate.

Proceed

204