Page 209 - Internal Auditing Standards

P. 209

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

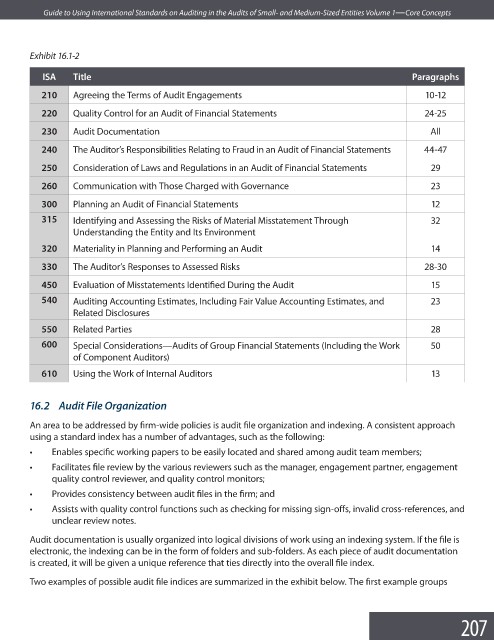

Exhibit 16.1-2

ISA Title Paragraphs

210 Agreeing the Terms of Audit Engagements 10-12

220 Quality Control for an Audit of Financial Statements 24-25

230 Audit Documentation All

240 The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements 44-47

250 Consideration of Laws and Regulations in an Audit of Financial Statements 29

260 Communication with Those Charged with Governance 23

300 Planning an Audit of Financial Statements 12

315 Identifying and Assessing the Risks of Material Misstatement Through 32

Understanding the Entity and Its Environment

320 Materiality in Planning and Performing an Audit 14

330 The Auditor’s Responses to Assessed Risks 28-30

450 Evaluation of Misstatements Identified During the Audit 15

540 Auditing Accounting Estimates, Including Fair Value Accounting Estimates, and 23

Related Disclosures

550 Related Parties 28

600 Special Considerations—Audits of Group Financial Statements (Including the Work 50

of Component Auditors)

610 Using the Work of Internal Auditors 13

16.2 Audit File Organization

An area to be addressed by firm-wide policies is audit file organization and indexing. A consistent approach

using a standard index has a number of advantages, such as the following:

• Enables specific working papers to be easily located and shared among audit team members;

• Facilitates file review by the various reviewers such as the manager, engagement partner, engagement

quality control reviewer, and quality control monitors;

• Provides consistency between audit files in the fi rm; and

• Assists with quality control functions such as checking for missing sign-offs, invalid cross-references, and

unclear review notes.

Audit documentation is usually organized into logical divisions of work using an indexing system. If the fi le is

electronic, the indexing can be in the form of folders and sub-folders. As each piece of audit documentation

is created, it will be given a unique reference that ties directly into the overall fi le index.

Two examples of possible audit file indices are summarized in the exhibit below. The first example groups

207