Page 198 - Internal Auditing Standards

P. 198

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

Where the objectives and scope of internal audit work includes a review of internal controls over fi nancial

reporting, the work of the internal auditor may (subject to its adequacy) be relied upon by the external auditor to

modify the nature and extent of the external auditor’s procedures. However, because internal auditors are hired

by the entity and form part of its internal control, they are not completely independent. Consequently, their work

would not be relied upon to the same extent as that performed by the external audit team.

Summary of Requirements

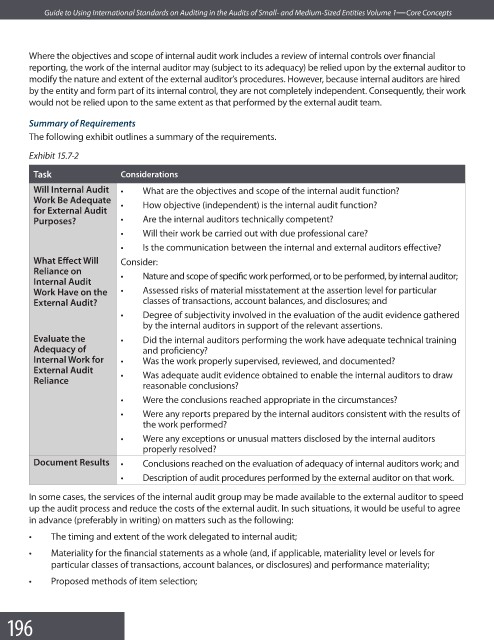

The following exhibit outlines a summary of the requirements.

Exhibit 15.7-2

Task Considerations

Will Internal Audit • What are the objectives and scope of the internal audit function?

Work Be Adequate • How objective (independent) is the internal audit function?

for External Audit

Purposes? • Are the internal auditors technically competent?

• Will their work be carried out with due professional care?

• Is the communication between the internal and external auditors eff ective?

What Eff ect Will Consider:

Reliance on • Nature and scope of specific work performed, or to be performed, by internal auditor;

Internal Audit

Work Have on the • Assessed risks of material misstatement at the assertion level for particular

External Audit? classes of transactions, account balances, and disclosures; and

• Degree of subjectivity involved in the evaluation of the audit evidence gathered

by the internal auditors in support of the relevant assertions.

Evaluate the • Did the internal auditors performing the work have adequate technical training

Adequacy of and profi ciency?

Internal Work for • Was the work properly supervised, reviewed, and documented?

External Audit

Reliance • Was adequate audit evidence obtained to enable the internal auditors to draw

reasonable conclusions?

• Were the conclusions reached appropriate in the circumstances?

• Were any reports prepared by the internal auditors consistent with the results of

the work performed?

• Were any exceptions or unusual matters disclosed by the internal auditors

properly resolved?

Document Results • Conclusions reached on the evaluation of adequacy of internal auditors work; and

• Description of audit procedures performed by the external auditor on that work.

In some cases, the services of the internal audit group may be made available to the external auditor to speed

up the audit process and reduce the costs of the external audit. In such situations, it would be useful to agree

in advance (preferably in writing) on matters such as the following:

• The timing and extent of the work delegated to internal audit;

• Materiality for the financial statements as a whole (and, if applicable, materiality level or levels for

particular classes of transactions, account balances, or disclosures) and performance materiality;

• Proposed methods of item selection;

196