Page 196 - Internal Auditing Standards

P. 196

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

Summarized Extracts from the Requirements Section

Documentation The group engagement team shall include in the audit documentation the following matters:

600.50

• An analysis of components, indicating those that are significant, and the type of

work performed on the financial information of the components;

• The nature, timing, and extent of the group engagement team’s involvement in the

work performed by the component auditors on significant components, including,

where applicable, the group engagement team’s review of relevant parts of the

component auditors’ audit documentation and conclusions thereon; and

• Written communications between the group engagement team and the

component auditors about the group engagement team’s requirements.

15.7 ISA 610 — Using the Work of Internal Auditors

Paragraph # ISA Objective(s)

610.6 The objectives of the external auditor, where the entity has an internal audit function that the

external auditor has determined is likely to be relevant to the audit, are:

(a) To determine whether, and to what extent, to use specific work of the internal auditors;

and

(b) If using the specific work of the internal auditors, to determine whether that work is

adequate for the purposes of the audit.

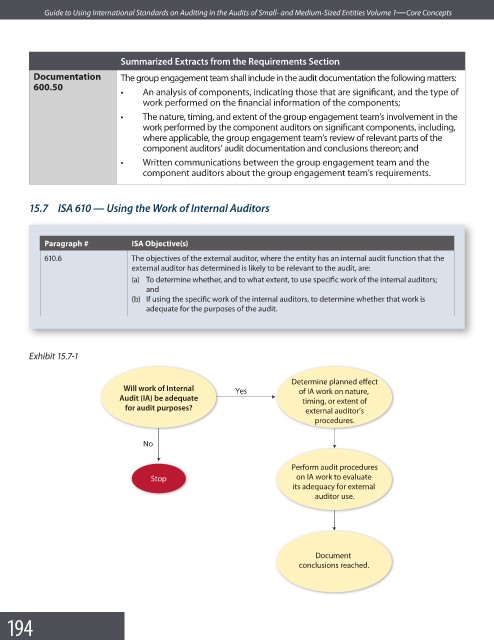

Exhibit 15.7-1

Determine planned effect

Will work of Internal Yes of IA work on nature,

Audit (IA) be adequate timing, or extent of

for audit purposes? external auditor’s

procedures.

No

Perform audit procedures

Stop on IA work to evaluate

its adequacy for external

auditor use.

Document

conclusions reached.

194