Page 192 - Internal Auditing Standards

P. 192

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

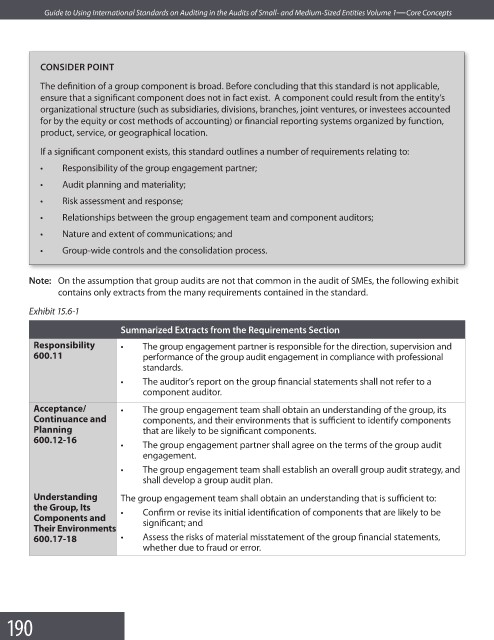

CONSIDER POINT

The definition of a group component is broad. Before concluding that this standard is not applicable,

ensure that a significant component does not in fact exist. A component could result from the entity’s

organizational structure (such as subsidiaries, divisions, branches, joint ventures, or investees accounted

for by the equity or cost methods of accounting) or financial reporting systems organized by function,

product, service, or geographical location.

If a significant component exists, this standard outlines a number of requirements relating to:

• Responsibility of the group engagement partner;

• Audit planning and materiality;

• Risk assessment and response;

• Relationships between the group engagement team and component auditors;

• Nature and extent of communications; and

• Group-wide controls and the consolidation process.

Note: On the assumption that group audits are not that common in the audit of SMEs, the following exhibit

contains only extracts from the many requirements contained in the standard.

Exhibit 15.6-1

Summarized Extracts from the Requirements Section

Responsibility • The group engagement partner is responsible for the direction, supervision and

600.11 performance of the group audit engagement in compliance with professional

standards.

• The auditor’s report on the group financial statements shall not refer to a

component auditor.

Acceptance/ • The group engagement team shall obtain an understanding of the group, its

Continuance and components, and their environments that is sufficient to identify components

Planning that are likely to be signifi cant components.

600.12-16

• The group engagement partner shall agree on the terms of the group audit

engagement.

• The group engagement team shall establish an overall group audit strategy, and

shall develop a group audit plan.

Understanding The group engagement team shall obtain an understanding that is suffi cient to:

the Group, Its • Confirm or revise its initial identification of components that are likely to be

Components and signifi cant; and

Their Environments

600.17-18 • Assess the risks of material misstatement of the group fi nancial statements,

whether due to fraud or error.

190