Page 220 - Internal Auditing Standards

P. 220

17. Forming an Opinion on Financial

Statements

Chapter Content Relevant ISAs

Requirements and considerations related to: 700

• Forming an opinion on the financial statements; and

• Preparing an appropriately worded auditor’s report.

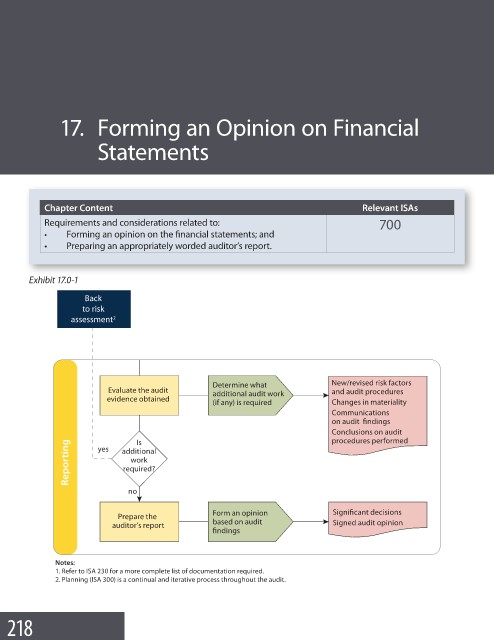

Exhibit 17.0-1

Back

to risk

assessment 2

Determine what New/revised risk factors

Evaluate the audit additional audit work and audit procedures

evidence obtained

(if any) is required Changes in materiality

Communications

on audit findings

Conclusions on audit

procedures performed

Is

Reporting yes additional

work

required?

no

Form an opinion Significant decisions

Prepare the

auditor’s report based on audit Signed audit opinion

findings

Notes:

1. Refer to ISA 230 for a more complete list of documentation required.

2. Planning (ISA 300) is a continual and iterative process throughout the audit.

218