Page 224 - Internal Auditing Standards

P. 224

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

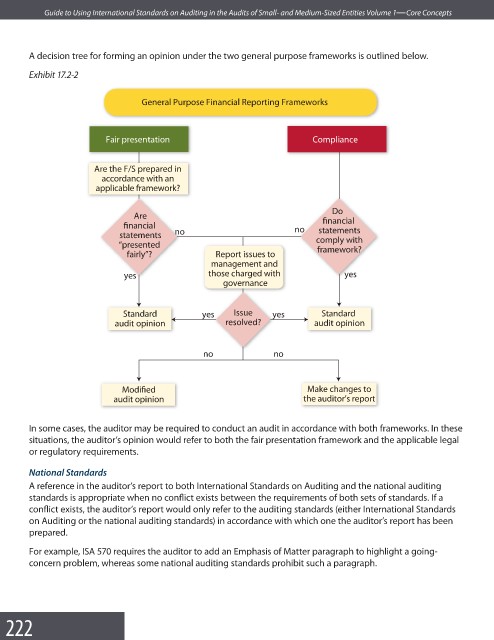

A decision tree for forming an opinion under the two general purpose frameworks is outlined below.

Exhibit 17.2-2

General Purpose Financial Reporting Frameworks

Fair presentation Compliance

Are the F/S prepared in

accordance with an

applicable framework?

Do

Are

financial no financial

statements

statements no comply with

“presented framework?

fairly”? Report issues to

management and

yes those charged with yes

governance

Standard yes Issue yes Standard

audit opinion resolved? audit opinion

no no

Modified Make changes to

audit opinion the auditor’s report

In some cases, the auditor may be required to conduct an audit in accordance with both frameworks. In these

situations, the auditor’s opinion would refer to both the fair presentation framework and the applicable legal

or regulatory requirements.

National Standards

A reference in the auditor’s report to both International Standards on Auditing and the national auditing

standards is appropriate when no conflict exists between the requirements of both sets of standards. If a

conflict exists, the auditor’s report would only refer to the auditing standards (either International Standards

on Auditing or the national auditing standards) in accordance with which one the auditor’s report has been

prepared.

For example, ISA 570 requires the auditor to add an Emphasis of Matter paragraph to highlight a going-

concern problem, whereas some national auditing standards prohibit such a paragraph.

222