Page 227 - Internal Auditing Standards

P. 227

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

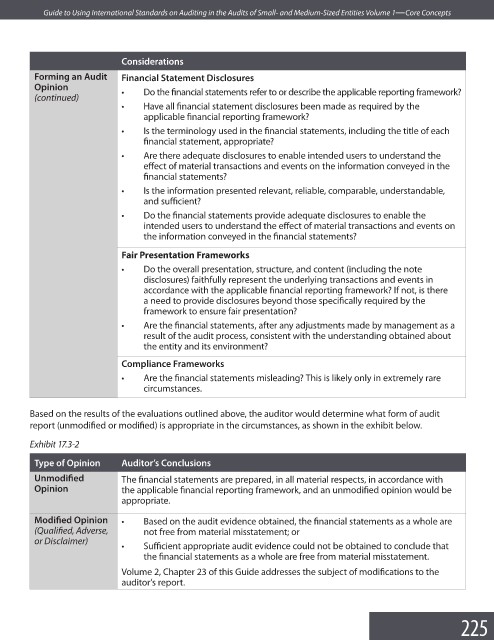

Considerations

Forming an Audit Financial Statement Disclosures

Opinion • Do the financial statements refer to or describe the applicable reporting framework?

(continued)

• Have all financial statement disclosures been made as required by the

applicable financial reporting framework?

• Is the terminology used in the financial statements, including the title of each

financial statement, appropriate?

• Are there adequate disclosures to enable intended users to understand the

effect of material transactions and events on the information conveyed in the

fi nancial statements?

• Is the information presented relevant, reliable, comparable, understandable,

and suffi cient?

• Do the financial statements provide adequate disclosures to enable the

intended users to understand the effect of material transactions and events on

the information conveyed in the fi nancial statements?

Fair Presentation Frameworks

• Do the overall presentation, structure, and content (including the note

disclosures) faithfully represent the underlying transactions and events in

accordance with the applicable financial reporting framework? If not, is there

a need to provide disclosures beyond those specifically required by the

framework to ensure fair presentation?

• Are the financial statements, after any adjustments made by management as a

result of the audit process, consistent with the understanding obtained about

the entity and its environment?

Compliance Frameworks

• Are the financial statements misleading? This is likely only in extremely rare

circumstances.

Based on the results of the evaluations outlined above, the auditor would determine what form of audit

report (unmodified or modified) is appropriate in the circumstances, as shown in the exhibit below.

Exhibit 17.3-2

Type of Opinion Auditor’s Conclusions

Unmodifi ed The financial statements are prepared, in all material respects, in accordance with

Opinion the applicable financial reporting framework, and an unmodified opinion would be

appropriate.

Modifi ed Opinion • Based on the audit evidence obtained, the financial statements as a whole are

(Qualifi ed, Adverse, not free from material misstatement; or

or Disclaimer)

• Sufficient appropriate audit evidence could not be obtained to conclude that

the financial statements as a whole are free from material misstatement.

Volume 2, Chapter 23 of this Guide addresses the subject of modifications to the

auditor’s report.

225