Page 231 - Internal Auditing Standards

P. 231

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

Paragraph # Relevant Extracts from ISAs

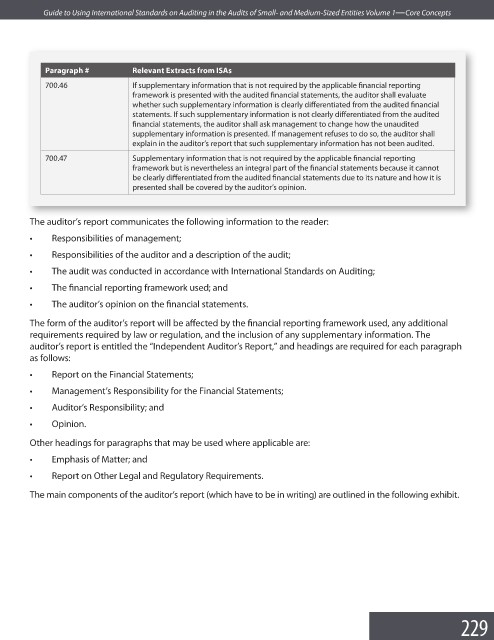

700.46 If supplementary information that is not required by the applicable fi nancial reporting

framework is presented with the audited financial statements, the auditor shall evaluate

whether such supplementary information is clearly differentiated from the audited fi nancial

statements. If such supplementary information is not clearly differentiated from the audited

financial statements, the auditor shall ask management to change how the unaudited

supplementary information is presented. If management refuses to do so, the auditor shall

explain in the auditor’s report that such supplementary information has not been audited.

700.47 Supplementary information that is not required by the applicable fi nancial reporting

framework but is nevertheless an integral part of the financial statements because it cannot

be clearly differentiated from the audited financial statements due to its nature and how it is

presented shall be covered by the auditor’s opinion.

The auditor’s report communicates the following information to the reader:

• Responsibilities of management;

• Responsibilities of the auditor and a description of the audit;

• The audit was conducted in accordance with International Standards on Auditing;

• The financial reporting framework used; and

• The auditor’s opinion on the fi nancial statements.

The form of the auditor’s report will be affected by the financial reporting framework used, any additional

requirements required by law or regulation, and the inclusion of any supplementary information. The

auditor’s report is entitled the “Independent Auditor’s Report,” and headings are required for each paragraph

as follows:

• Report on the Financial Statements;

• Management’s Responsibility for the Financial Statements;

• Auditor’s Responsibility; and

• Opinion.

Other headings for paragraphs that may be used where applicable are:

• Emphasis of Matter; and

• Report on Other Legal and Regulatory Requirements.

The main components of the auditor’s report (which have to be in writing) are outlined in the following exhibit.

229