Page 234 - Internal Auditing Standards

P. 234

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

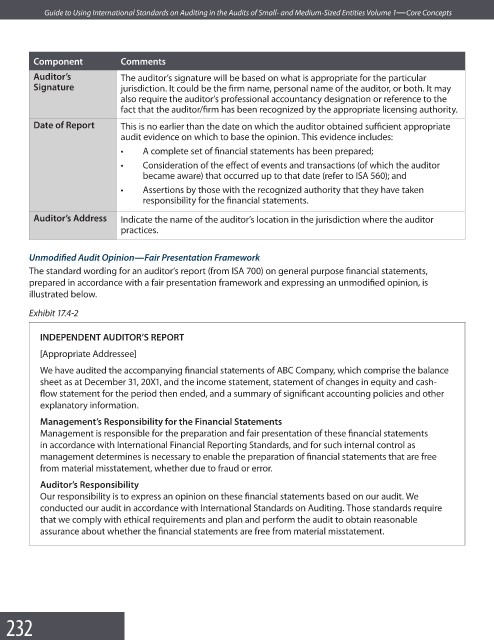

Component Comments

Auditor’s The auditor’s signature will be based on what is appropriate for the particular

Signature jurisdiction. It could be the firm name, personal name of the auditor, or both. It may

also require the auditor’s professional accountancy designation or reference to the

fact that the auditor/firm has been recognized by the appropriate licensing authority.

Date of Report This is no earlier than the date on which the auditor obtained suffi cient appropriate

audit evidence on which to base the opinion. This evidence includes:

• A complete set of financial statements has been prepared;

• Consideration of the effect of events and transactions (of which the auditor

became aware) that occurred up to that date (refer to ISA 560); and

• Assertions by those with the recognized authority that they have taken

responsibility for the fi nancial statements.

Auditor’s Address Indicate the name of the auditor’s location in the jurisdiction where the auditor

practices.

Unmodified Audit Opinion—Fair Presentation Framework

The standard wording for an auditor’s report (from ISA 700) on general purpose fi nancial statements,

prepared in accordance with a fair presentation framework and expressing an unmodified opinion, is

illustrated below.

Exhibit 17.4-2

INDEPENDENT AUDITOR’S REPORT

[Appropriate Addressee]

We have audited the accompanying financial statements of ABC Company, which comprise the balance

sheet as at December 31, 20X1, and the income statement, statement of changes in equity and cash-

flow statement for the period then ended, and a summary of significant accounting policies and other

explanatory information.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these fi nancial statements

in accordance with International Financial Reporting Standards, and for such internal control as

management determines is necessary to enable the preparation of financial statements that are free

from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We

conducted our audit in accordance with International Standards on Auditing. Those standards require

that we comply with ethical requirements and plan and perform the audit to obtain reasonable

assurance about whether the financial statements are free from material misstatement.

232