Page 57 - Internal Auditing Standards

P. 57

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

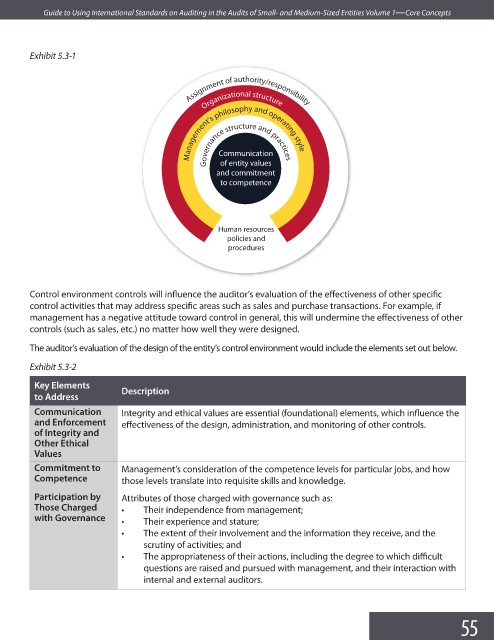

Exhibit 5.3-1

Assignment of authority/responsibility

Organizational structure

Management’s philosophy and operating style

Communication

of entity values

Governance structure and practices

and commitment

to competence

Human resources

policies and

procedures

Control environment controls will influence the auditor’s evaluation of the effectiveness of other specifi c

control activities that may address specific areas such as sales and purchase transactions. For example, if

management has a negative attitude toward control in general, this will undermine the effectiveness of other

controls (such as sales, etc.) no matter how well they were designed.

The auditor’s evaluation of the design of the entity’s control environment would include the elements set out below.

Exhibit 5.3-2

Key Elements

Description

to Address

Communication Integrity and ethical values are essential (foundational) elements, which infl uence the

and Enforcement effectiveness of the design, administration, and monitoring of other controls.

of Integrity and

Other Ethical

Values

Commitment to Management’s consideration of the competence levels for particular jobs, and how

Competence those levels translate into requisite skills and knowledge.

Participation by Attributes of those charged with governance such as:

Those Charged • Their independence from management;

with Governance • Their experience and stature;

• The extent of their involvement and the information they receive, and the

scrutiny of activities; and

• The appropriateness of their actions, including the degree to which diffi cult

questions are raised and pursued with management, and their interaction with

internal and external auditors.

55