Page 52 - Internal Auditing Standards

P. 52

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

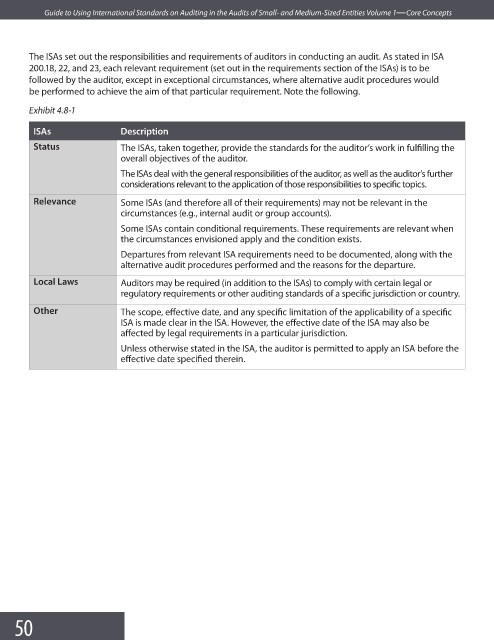

The ISAs set out the responsibilities and requirements of auditors in conducting an audit. As stated in ISA

200.18, 22, and 23, each relevant requirement (set out in the requirements section of the ISAs) is to be

followed by the auditor, except in exceptional circumstances, where alternative audit procedures would

be performed to achieve the aim of that particular requirement. Note the following.

Exhibit 4.8-1

ISAs Description

Status The ISAs, taken together, provide the standards for the auditor’s work in fulfi lling the

overall objectives of the auditor.

The ISAs deal with the general responsibilities of the auditor, as well as the auditor’s further

considerations relevant to the application of those responsibilities to specifi c topics.

Relevance Some ISAs (and therefore all of their requirements) may not be relevant in the

circumstances (e.g., internal audit or group accounts).

Some ISAs contain conditional requirements. These requirements are relevant when

the circumstances envisioned apply and the condition exists.

Departures from relevant ISA requirements need to be documented, along with the

alternative audit procedures performed and the reasons for the departure.

Local Laws Auditors may be required (in addition to the ISAs) to comply with certain legal or

regulatory requirements or other auditing standards of a specific jurisdiction or country.

Other The scope, effective date, and any specific limitation of the applicability of a specifi c

ISA is made clear in the ISA. However, the effective date of the ISA may also be

affected by legal requirements in a particular jurisdiction.

Unless otherwise stated in the ISA, the auditor is permitted to apply an ISA before the

effective date specifi ed therein.

50