Page 51 - Internal Auditing Standards

P. 51

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

completion of such reviews occurred before the audit report was dated,

– Communication has been made to the appropriate personnel about deficiencies that have been

identifi ed, and

– Appropriate follow-up has been made to ensure that identifi ed deficiencies in quality have been

addressed on a timely basis.

• Cyclical completed fi le inspections

The ongoing consideration and evaluation of the firm’s system of quality control includes a cyclical

inspection of at least one completed engagement file for each partner. This is required to ensure

compliance with professional/legal requirements, and that assurance reports being issued are

appropriate in the circumstances. Cyclical inspections help to identify deficiencies and training needs,

and enable the firm to make necessary changes, on a timely basis.

Upon completion of the review, the monitor would prepare a report that, after discussion with the partners,

would be communicated to all managers and professional staff along with the action steps to be taken.

Who can be appointed as monitor?

• Monitoring of fi rm-level policies

The review of compliance with the firm’s policies would be performed by a suitably qualified person who

ideally is not also responsible for managing or developing quality control within the firm. However, ISQC 1

recognizes that this may not always be possible in smaller firms, so self-monitoring is acceptable. Alternatively,

an individual external to the firm, with the competence and capabilities to act as an engagement partner,

could be appointed. This would enhance the independence and objectivity of the fi rm.

• Completed fi le inspections

The person appointed to inspect completed engagement files must be suitably qualified, and must not

have been involved in performing the engagement or the engagement quality control review on the fi le.

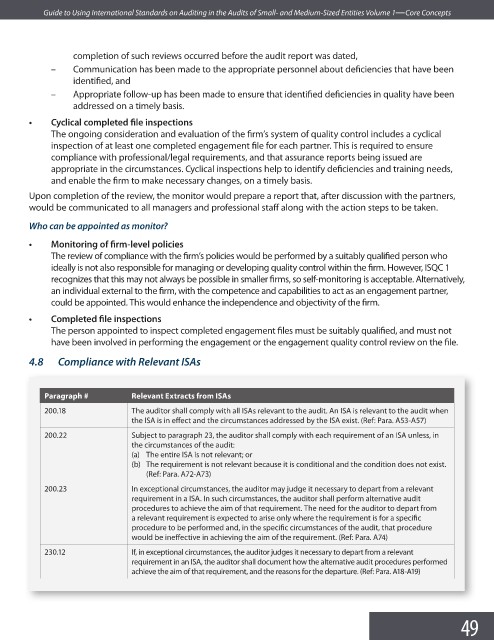

4.8 Compliance with Relevant ISAs

Paragraph # Relevant Extracts from ISAs

200.18 The auditor shall comply with all ISAs relevant to the audit. An ISA is relevant to the audit when

the ISA is in effect and the circumstances addressed by the ISA exist. (Ref: Para. A53-A57)

200.22 Subject to paragraph 23, the auditor shall comply with each requirement of an ISA unless, in

the circumstances of the audit:

(a) The entire ISA is not relevant; or

(b) The requirement is not relevant because it is conditional and the condition does not exist.

(Ref: Para. A72-A73)

200.23 In exceptional circumstances, the auditor may judge it necessary to depart from a relevant

requirement in a ISA. In such circumstances, the auditor shall perform alternative audit

procedures to achieve the aim of that requirement. The need for the auditor to depart from

a relevant requirement is expected to arise only where the requirement is for a specifi c

procedure to be performed and, in the specific circumstances of the audit, that procedure

would be ineffective in achieving the aim of the requirement. (Ref: Para. A74)

230.12 If, in exceptional circumstances, the auditor judges it necessary to depart from a relevant

requirement in an ISA, the auditor shall document how the alternative audit procedures performed

achieve the aim of that requirement, and the reasons for the departure. (Ref: Para. A18-A19)

49