Page 50 - Internal Auditing Standards

P. 50

Guide to Using International Standards on Auditing in the Audits of Small- and Medium-Sized Entities Volume 1—Core Concepts

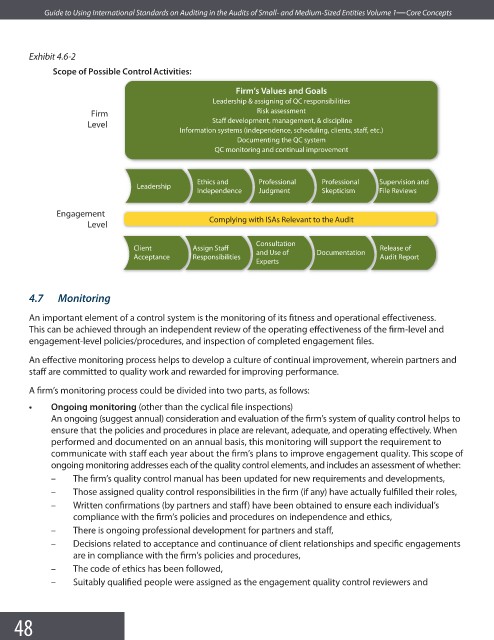

Exhibit 4.6-2

Scope of Possible Control Activities:

Firm’s Values and Goals

Leadership & assigning of QC responsibilities

Firm Risk assessment

Staff development, management, & discipline

Level

Information systems (independence, scheduling, clients, staff, etc.)

Documenting the QC system

QC monitoring and continual improvement

Ethics and Professional Professional Supervision and

Leadership

Independence Judgment Skepticism File Reviews

Engagement

Complying with ISAs Relevant to the Audit

Level

Consultation

Client Assign Staff and Use of Documentation Release of

Acceptance Responsibilities Audit Report

Experts

4.7 Monitoring

An important element of a control system is the monitoring of its fitness and operational eff ectiveness.

This can be achieved through an independent review of the operating effectiveness of the fi rm-level and

engagement-level policies/procedures, and inspection of completed engagement fi les.

An effective monitoring process helps to develop a culture of continual improvement, wherein partners and

staff are committed to quality work and rewarded for improving performance.

A firm’s monitoring process could be divided into two parts, as follows:

• Ongoing monitoring (other than the cyclical fi le inspections)

An ongoing (suggest annual) consideration and evaluation of the firm’s system of quality control helps to

ensure that the policies and procedures in place are relevant, adequate, and operating eff ectively. When

performed and documented on an annual basis, this monitoring will support the requirement to

communicate with staff each year about the firm’s plans to improve engagement quality. This scope of

ongoing monitoring addresses each of the quality control elements, and includes an assessment of whether:

– The firm’s quality control manual has been updated for new requirements and developments,

– Those assigned quality control responsibilities in the firm (if any) have actually fulfilled their roles,

– Written confirmations (by partners and staff) have been obtained to ensure each individual’s

compliance with the firm’s policies and procedures on independence and ethics,

– There is ongoing professional development for partners and staff ,

– Decisions related to acceptance and continuance of client relationships and specifi c engagements

are in compliance with the firm’s policies and procedures,

– The code of ethics has been followed,

– Suitably qualified people were assigned as the engagement quality control reviewers and

48