Page 53 - Internal Auditing Standards

P. 53

5. Internal Control — Purpose

and Components

Chapter Content Relevant ISA

To outline the purpose, scope, and nature of internal control over

financial reporting, including the five components to be evaluated by 315

the auditor.

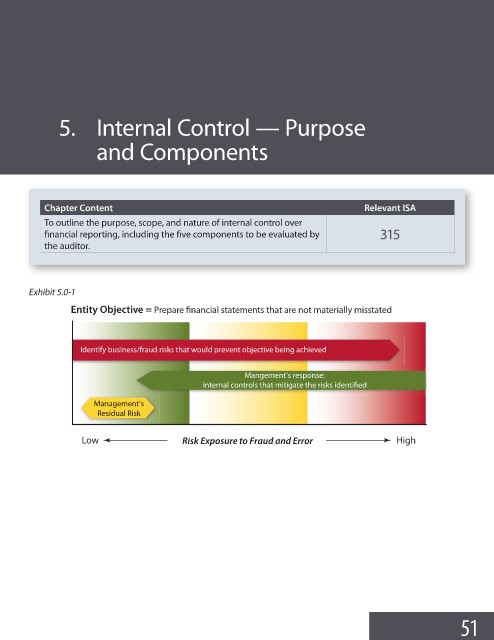

Exhibit 5.0-1

Entity Objective = Prepare financial statements that are not materially misstated

Identify business/fraud risks that would prevent objective being achieved

Mangement’s response:

internal controls that mitigate the risks identified

Management’s

Residual Risk

Low Risk Exposure to Fraud and Error High

51