Page 525 - ITGC_Audit Guides

P. 525

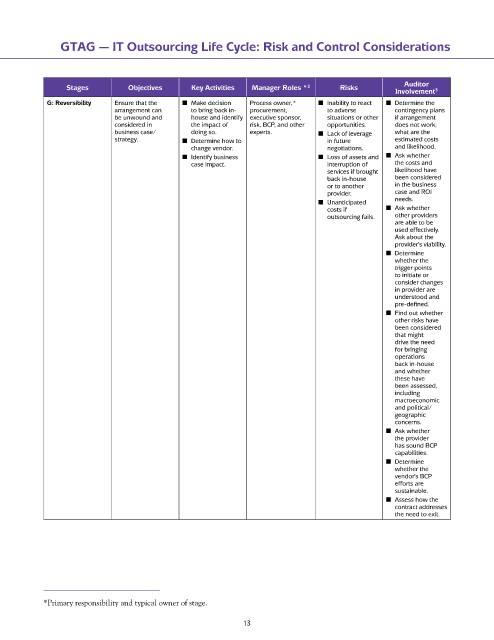

GTAG — IT Outsourcing Life Cycle: Risk and Control Considerations

Stages Objectives Key Activities Manager Roles * 2 Risks Auditor

Involvement 3

G: Reversibility Ensure that the n Make decision Process owner,* n Inability to react n Determine the

arrangement can to bring back in- procurement, to adverse contingency plans

be unwound and house and identify executive sponsor, situations or other if arrangement

considered in the impact of risk, BCP, and other opportunities. does not work;

business case/ doing so. experts. n Lack of leverage what are the

strategy. n Determine how to in future estimated costs

change vendor. negotiations. and likelihood.

n Identify business n Loss of assets and n Ask whether

case impact. interruption of the costs and

services if brought likelihood have

back in-house been considered

or to another in the business

provider. case and ROI

n Unanticipated needs.

costs if n Ask whether

outsourcing fails. other providers

are able to be

used effectively.

Ask about the

provider’s viability.

n Determine

whether the

trigger points

to initiate or

consider changes

in provider are

understood and

pre-defined.

n Find out whether

other risks have

been considered

that might

drive the need

for bringing

operations

back in-house

and whether

these have

been assessed,

including

macroeconomic

and political/

geographic

concerns.

n Ask whether

the provider

has sound BCP

capabilities.

n Determine

whether the

vendor’s BCP

efforts are

sustainable.

n Assess how the

contract addresses

the need to exit.

*Primary responsibility and typical owner of stage.

13