Page 639 - TaxAdviser_2022

P. 639

EXPENSES & DEDUCTIONS

beyond that mandated by Sec. 199A(b)

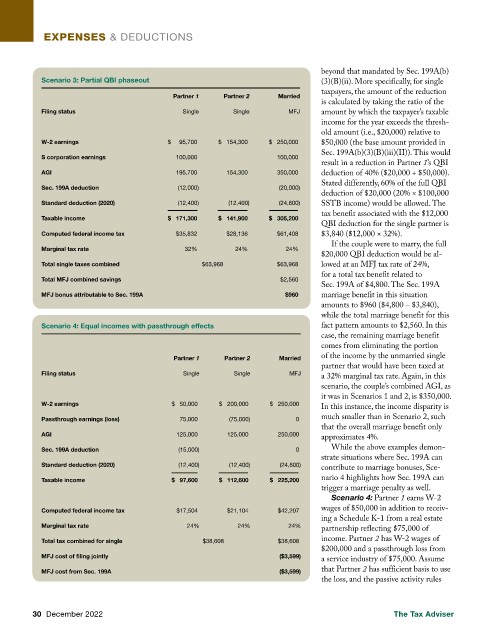

Scenario 3: Partial QBI phaseout (3)(B)(ii). More specifically, for single

taxpayers, the amount of the reduction

Partner 1 Partner 2 Married

is calculated by taking the ratio of the

Filing status Single Single MFJ amount by which the taxpayer’s taxable

income for the year exceeds the thresh-

old amount (i.e., $20,000) relative to

W-2 earnings $ 95,700 $ 154,300 $ 250,000 $50,000 (the base amount provided in

Sec. 199A(b)(3)(B)(iii)(II)). This would

S corporation earnings 100,000 100,000

result in a reduction in Partner 1’s QBI

AGI 195,700 154,300 350,000 deduction of 40% ($20,000 ÷ $50,000).

Stated differently, 60% of the full QBI

Sec. 199A deduction (12,000) (20,000)

deduction of $20,000 (20% × $100,000

Standard deduction (2020) (12,400) (12,400) (24,800) SSTB income) would be allowed. The

tax benefit associated with the $12,000

Taxable income $ 171,300 $ 141,900 $ 305,200

QBI deduction for the single partner is

Computed federal income tax $35,832 $28,136 $61,408 $3,840 ($12,000 × 32%).

If the couple were to marry, the full

Marginal tax rate 32% 24% 24%

$20,000 QBI deduction would be al-

Total single taxes combined $63,968 $63,968 lowed at an MFJ tax rate of 24%,

for a total tax benefit related to

Total MFJ combined savings $2,560

Sec. 199A of $4,800. The Sec. 199A

MFJ bonus attributable to Sec. 199A $960 marriage benefit in this situation

amounts to $960 ($4,800 – $3,840),

while the total marriage benefit for this

Scenario 4: Equal incomes with passthrough effects fact pattern amounts to $2,560. In this

case, the remaining marriage benefit

comes from eliminating the portion

Partner 1 Partner 2 Married of the income by the unmarried single

partner that would have been taxed at

Filing status Single Single MFJ a 32% marginal tax rate. Again, in this

scenario, the couple’s combined AGI, as

it was in Scenarios 1 and 2, is $350,000.

W-2 earnings $ 50,000 $ 200,000 $ 250,000 In this instance, the income disparity is

Passthrough earnings (loss) 75,000 (75,000) 0 much smaller than in Scenario 2, such

that the overall marriage benefit only

AGI 125,000 125,000 250,000 approximates 4%.

Sec. 199A deduction (15,000) 0 While the above examples demon-

strate situations where Sec. 199A can

Standard deduction (2020) (12,400) (12,400) (24,800) contribute to marriage bonuses, Sce-

Taxable income $ 97,600 $ 112,600 $ 225,200 nario 4 highlights how Sec. 199A can

trigger a marriage penalty as well.

Scenario 4: Partner 1 earns W-2

Computed federal income tax $17,504 $21,104 $42,207 wages of $50,000 in addition to receiv-

ing a Schedule K-1 from a real estate

Marginal tax rate 24% 24% 24% partnership reflecting $75,000 of

Total tax combined for single $38,608 $38,608 income. Partner 2 has W-2 wages of

$200,000 and a passthrough loss from

MFJ cost of filing jointly ($3,599)

a service industry of $75,000. Assume

MFJ cost from Sec. 199A ($3,599) that Partner 2 has sufficient basis to use

the loss, and the passive activity rules

30 December 2022 The Tax Adviser