Page 432 - Large Business IRS Training Guides

P. 432

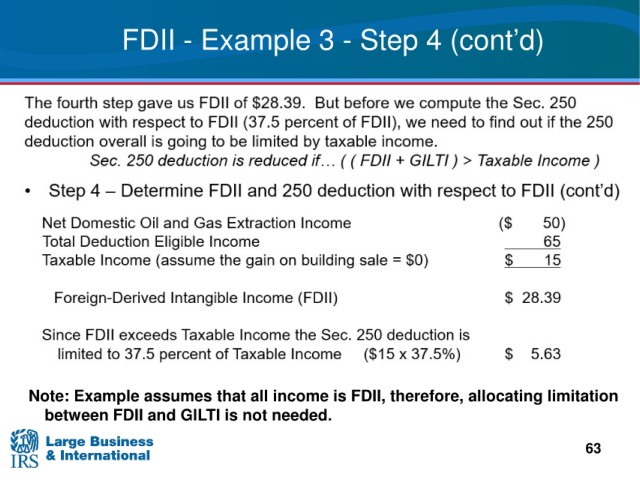

FDII - Example 3 - Step 4 (cont’d)

all income is FDII, therefore, allocating limitation

Note: Example assumes that

between

FDII and GILTI is not needed.

63